If you’re searching for ways to secure your wealth, and protect your family’s assets from lawsuits, trusts can be the solution you need. But how do trusts work? This article explores everything you need to know, from the basics of trusts to advanced strategies like Asset Protection Trusts and the innovative Bridge Trust®.

Whether you’re an entrepreneur, professional, or family looking to protect your legacy, this guide offers clear explanations and actionable insights.

What Is a Trust?

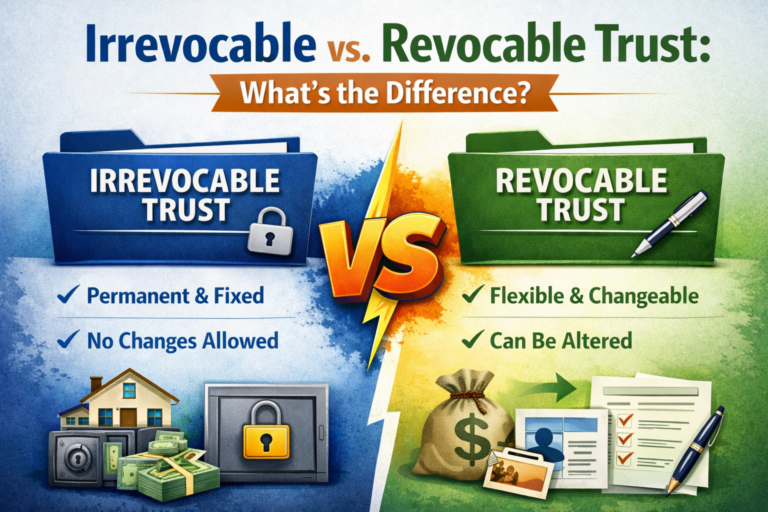

A trust is a legal agreement where one person (the Settlor) transfers assets to another person or entity (the Trustee) to manage for the benefit of someone else (the Beneficiary). Trusts offer financial protection, estate planning benefits, and even asset protection from creditors or lawsuits.

Key Components of a Trust

1. Settlor: The individual who creates the trust and transfers assets into it.

2. Trustee: The person or institution responsible for managing the assets.

3. Beneficiary: The individual(s) who benefit from the trust assets.

4. Provisions: The rules for managing and distributing the trust assets.

A Brief History of Asset Protection

The concept of Asset Protection as a distinct area of law is relatively new. When Gary Lodmell began practicing law in 1969, the legal system was far more structured to prevent lawsuits. There were four key “pillars” that minimized litigation:

1. No Contingent Fees: Attorneys couldn’t accept fees contingent on winning a case.

2. No Advertising: Lawyers were prohibited from marketing their services.

3. No Frivolous Lawsuits: Strict ethical standards limited baseless legal actions.

4. Strict Civil Procedure Rules: Lawsuits required clear, stated causes of action.

By the 1980s, these pillars began to erode:

• 1964: Contingent fees became universally accepted.

• 1977: The U.S. Supreme Court allowed attorney advertising (Bates v. State Bar of Arizona).

• 1983: The ABA revised ethics rules, loosening the definition of frivolous lawsuits.

• 1980-2000: Changes in civil procedure allowed weaker cases to proceed.

As lawsuits surged, business owners and entrepreneurs sought ways to protect their assets. The 1980s saw the emergence of Asset Protection Trusts (APTs), designed to shield wealth from legal threats. These trusts marked a turning point, evolving into both Domestic Asset Protection Trusts (DAPTs) and International Asset Protection Trusts (IAPTs), offering solutions tailored to different risk profiles.

How Trusts Work: A Simple Example

Imagine giving your uncle $1,000 to hold for your son for 10 years. You instruct him to:

• Invest the money.

• Use it only for your son’s benefit.

• Avoid giving the money directly if creditors come after your son.

This arrangement creates a Spendthrift Trust, designed to protect assets from creditors. Spendthrift provisions prevent beneficiaries or courts from accessing the assets directly.

The Rise of International Asset Protection Trusts

By the late 1980s, offshore jurisdictions like the Cook Islands revolutionized asset protection. The Cook Islands Trust Act of 1984 introduced unparalleled safeguards:

1. Exclusive jurisdiction to Cook Islands courts.

2. A 2-year statute of limitations for claims.

3. High burdens of proof for lawsuits (“beyond a reasonable doubt”).

4. Prohibitions on recognizing foreign judgments, including U.S. court orders.

These features made Cook Islands Trusts the gold standard for protecting wealth internationally.

The Bridge Trust®: Combining Domestic and Offshore Strengths

Though offshore trusts, and specifically the Cook Islands Trust, provide the most robust protection, many people hesitate to relinquish control over their assets. The Bridge Trust®, developed in 1997, combines domestic and offshore benefits for ultimate flexibility and security.

Key Features of the Bridge Trust®

1. Dual Jurisdiction: The trust is domestic until a legal threat arises, at which point it transitions offshore.

2. Settlor Control: The Settlor retains control as Trustee unless an “event of duress” occurs.

3. Tax Efficiency: Classified as a domestic trust for U.S. tax purposes, avoiding extra filings.

4. Cost-Effective: Annual fees of $1,495.

The Bridge Trust® has become a preferred choice for entrepreneurs, professionals, and families who want the best of both worlds: control during normal circumstances and protection during crises.

Benefits of Trusts in Asset Protection

1. Legal Protection: Trusts create a legal barrier between your assets and creditors.

2. Tax Efficiency: Reduce estate taxes and protect generational wealth.

3. Flexibility: Customize provisions to suit family needs, including spendthrift clauses for irresponsible beneficiaries.

4. Privacy: Trusts keep your financial affairs private, unlike wills, which go through probate.

Conclusion

Asset Protection Trusts are one of the most powerful tools for protecting assets and ensuring your family’s financial security for generations to come. Whether you need a straightforward Self-Settled Spendthrift Trust, a fully foreign offshore asset protection trust like a Cook Islands Trust, or a hybrid asset protection trust like the Bridge Trust®, there’s a trust strategy tailored to your unique circumstances.

Understanding the distinctions between domestic and offshore trusts, the historical evolution of asset protection, and the pros and cons they provide ensures you make informed decisions. Choosing the right trust type and working with an experienced asset protection attorney is essential to maximizing your wealth’s safety and flexibility. Read my article on How to Choose the Right Asset Protection Attorney.

If you’re ready to explore the best trust options for your financial situation, consult with a knowledgeable asset protection attorney today. Whether you’re an entrepreneur, a professional, or a family looking to secure your legacy, a trust could be the most critical investment you make for your future.

For a legal consultation call (888) 773-9399 to talk with an asset protection attorney.

By: Brian T. Bradley, Esq.