Marcus owned twelve rental properties spread across four states.

Washington. Texas. Florida. Arizona. Three properties in each. Each state had its own LLC — formed locally to match the jurisdiction where the properties sat. He had done that part correctly. His stock portfolio was pushing $3 million. He held passive limited-partner interests in three syndications.

By any measure, Marcus had built something substantial.

What he did not have was a structure above the LLCs.

Everything flowed up to him personally. The LLC membership interests were assets he owned. The brokerage account was in his name. The syndication K-1s reported income directly to his Social Security number.

When a tenant injury lawsuit in Texas produced a jury verdict exceeding his insurance coverage by $1.4 million, the plaintiff’s attorney requested financial disclosures and began mapping Marcus’s balance sheet.

Marcus’s first question during his legal consultation was the same one most investors ask:

“Can’t I just form a Wyoming LLC as a management company and put everything under that?”

⸻

Why the Wyoming LLC Answer Is the Wrong Question

Wyoming LLCs do offer real advantages.

Wyoming requires no public disclosure of member names, maintains investor-friendly statutes, and provides genuine privacy benefits. For investors who want anonymity in ownership records, Wyoming can be a useful tool.

But Marcus wasn’t asking about privacy.

He was asking about protection.

And those are two very different things.

A Wyoming LLC formed as a management company above Marcus’s state LLCs runs into a fundamental issue: enforcement jurisdiction follows the debtor, not the entity.

Courts typically apply the forum state’s enforcement procedures when determining how a judgment creditor may reach a debtor’s assets. That means a creditor enforcing a Texas judgment against Marcus may ask a Texas court what remedies are available under Texas enforcement law, even if the entity holding the asset was formed in another state.

Marcus would own and manage the Wyoming LLC himself. In single-member structures like this, courts often conclude that the policy rationale behind charging-order protection — protecting innocent co-members from disruption — does not apply.

In Olmstead v. FTC, 44 So. 3d 76 (Fla. 2010), the Florida Supreme Court allowed a creditor to reach a debtor’s single-member LLC interest because there were no other members whose interests needed protection. Courts in other jurisdictions have applied similar reasoning when evaluating single-member entities.

The Wyoming LLC as a management company therefore gives Marcus an additional entity.

But it does not meaningfully change what courts can compel.

Once Marcus understood that distinction, his second question came quickly:

“So what do you use instead?”

The Limited Partnership as the Management Company

Most investors are familiar with limited partnerships from the outside.

They have participated in real estate syndications as limited partners. They contributed capital, received periodic K-1s, had no management authority, and understood their liability was limited to their investment.

What many investors never consider is using that same statutory structure inside their own asset-protection architecture.

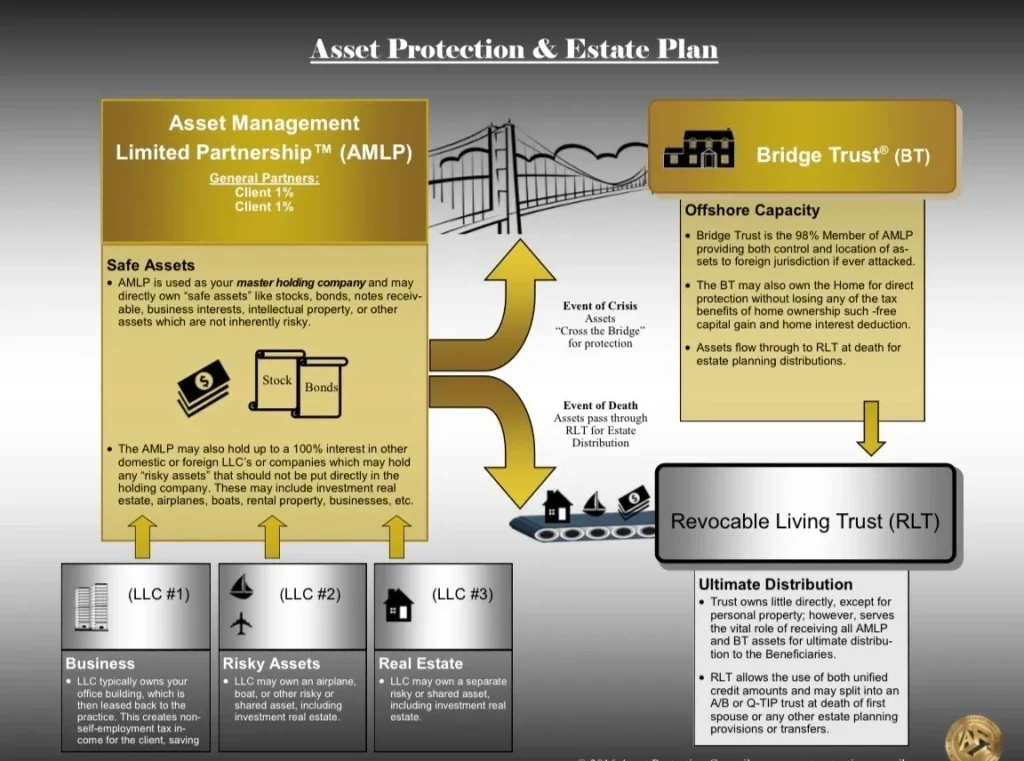

That is precisely what the Asset Management Limited Partnership (AMLP) is designed to do.

The AMLP is an Arizona limited partnership that functions as the master holding company and management hub for the entire structure. It sits above the operating LLCs and owns their membership interests. It can also hold brokerage assets, syndication interests, and other investment positions as a centralized ownership vehicle.

Because the entity is a limited partnership rather than an LLC, the legal relationship between Marcus and his assets changes.

In the AMLP structure:

• Marcus serves as a general partner, responsible for management decisions.

• The Bridge Trust® serves as the 98% limited partner, holding the equity ownership.

This separation matters.

Marcus’s personal balance sheet is no longer defined by direct ownership of the underlying assets. Instead, his role is primarily managerial.

That distinction becomes critical when a creditor attempts to enforce a judgment.

A creditor holding a judgment against Marcus personally cannot seize the AMLP’s underlying assets. They cannot directly reach the operating LLCs, brokerage accounts, or partnership investments held by the AMLP.

The statutory remedy available under Arizona law is a charging order against Marcus’s partnership interest.

A charging order grants the creditor the right to receive distributions if and when they are made.

It does not grant control over the partnership, management authority, or access to the underlying assets.

⸻

Why Arizona Is Used for the Limited Partnership

The choice of Arizona is not arbitrary.

Arizona partnership law includes specific statutory features that make it well suited for this role in a layered structure.

Under A.R.S. § 29-3503, a creditor’s remedy against a partner’s interest is generally limited to a charging order. The creditor does not obtain voting rights or management authority and cannot force liquidation of the partnership’s assets.

Arizona partnership statutes also allow partnership agreements to define events that trigger changes in partner status or rights.

When these provisions are drafted and implemented well before any creditor issues arise, courts typically treat them as contractual governance mechanisms rather than post-claim asset transfers.

In NextGear Capital v. Owens (Ariz. Ct. App. 2023), the Arizona Court of Appeals confirmed that charging orders do not grant management rights and that creditor remedies remain limited by the partnership statute.

This is an important structural distinction from the Wyoming LLC scenario.

Rather than relying on an out-of-state statute being respected elsewhere, the AMLP is formed in the jurisdiction whose law governs the partnership itself.

What Changes for Marcus

Before implementing the structure, Marcus’s balance sheet was fully accessible.

His LLC membership interests were assets he owned personally. His brokerage account was in his name. His syndication K-1s identified him as the direct investor.

A judgment creditor could pursue those assets through ordinary enforcement procedures.

After restructuring, the same assets still exist.

But their ownership pathway changes.

The operating LLCs remain in the states where the properties are located. That first layer isolates operational liability between individual assets.

Above those entities sits the AMLP, which holds the membership interests in the LLCs as well as Marcus’s brokerage assets and syndication interests.

A judgment creditor pursuing Marcus personally can reach only his partnership interest through a charging order.

Above the AMLP sits the Bridge Trust®, which holds the majority limited-partner interest.

During normal operation, the Bridge Trust functions as a domestic grantor trust under IRC §§ 671–677 and § 7701, maintaining IRS transparency and tax compliance.

If enforcement pressure escalates significantly, control — not ownership — may shift to an independent offshore trustee under the trust’s governing instrument.

Jurisdictions such as the Cook Islands do not automatically recognize U.S. judgments and require independent local proceedings before enforcement can occur, including proof of fraud under a heightened evidentiary standard. What is the Bridge Trust: https://btblegal.com/blog-articles/f/what-is-the-bridge-trust

The debt against Marcus remains real.

What changes is what a creditor can compel through enforcement.

Tax and Lending Considerations

The AMLP can also provide structural advantages for investors managing larger portfolios.

Partnership structures allow guaranteed payments under IRC § 707, which are deductible to the partnership and taxable as income to the recipient partner.

Many LLC distributions, by contrast, are simply owner draws that do not create entity-level deductions.

When a management entity serves as the general partner and charges a management fee, that fee may be deductible to the partnership before income flows to the limited partners.

For financing purposes, lenders evaluating real-estate investors often rely heavily on partnership K-1 income when it shows consistent distributions, documented guaranteed payments, and a clear partnership balance sheet.

A partnership structure that produces stable K-1 history can therefore help present a clearer financial picture during underwriting.

⸻

The Takeaway

Marcus’s first instinct — forming a Wyoming LLC as a management company — reflects what many investors believe is the logical next step.

Wyoming does provide privacy advantages.

But privacy is not protection.

A single-member management LLC owned and controlled by the same individual does not fundamentally change what courts can compel when enforcing a judgment.

A limited partnership used as the second layer in a structure introduces something that an LLC does not always provide: statutory separation between ownership and management.

That separation changes how creditor remedies operate.

The AMLP sits at the center of the structure not because it is exotic, but because it aligns with long-standing partnership law designed to protect passive capital and preserve business continuity.

The properties remain where they are.

The equity remains real.

What changes is the path a creditor must follow to reach it.

You don’t fall to the level of your state of formation.

You fall to the level of your legal structure.

📞 Ready to build a real asset protection system? Call Bradley Legal Corp. at (888) 773-9399 to schedule your consultation. You don’t rise to the level of your income — you fall to the level of your legal structure.

By: Brian T. Bradley, Esq.