Florida is one of the most attractive states in the country to build wealth.

No state income tax. No state estate tax. No inheritance tax. A homestead exemption that is among the strongest in the nation. Favorable tenancy by the entireties protection for married couples.

On paper, it looks like a protected environment.

And that is exactly the problem.

Because the wealth environment Florida creates — accelerating net savings rates, compounding real estate appreciation, concentrated professional income — also creates two serious exposure problems that most Florida families at $15 million or more have never been shown simultaneously.

A creditor problem. And a generational tax problem.

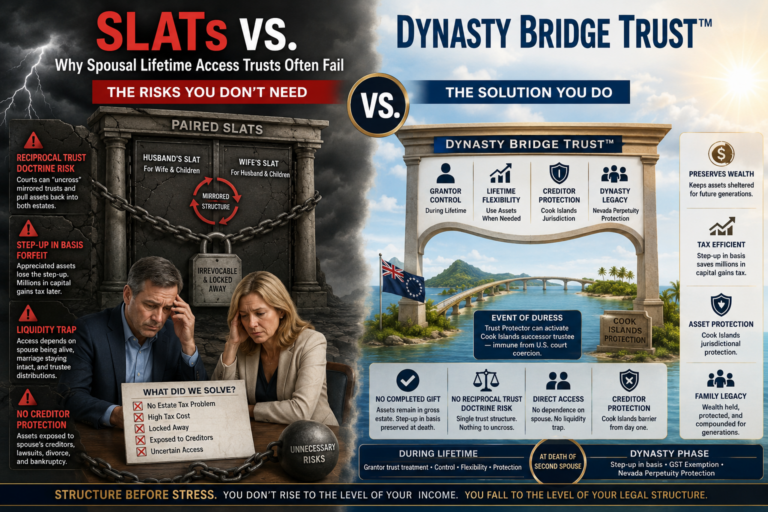

Most plans address one. The Dynasty Bridge Trust™ addresses both — inside one integrated structure.

The Florida Creditor Environment Is Not What Most People Think

Florida has a reputation for debtor-friendly exemptions. That reputation is partially earned. The homestead exemption is real. Tenancy by the entireties is real. Retirement plan protection is real.

What is not discussed enough is the other side of that equation.

Florida is one of the most plaintiff-friendly litigation environments in the country. The plaintiffs’ bar is aggressive, well-funded, and experienced at nuclear verdicts — particularly in medical malpractice, premises liability, construction defects, and personal guarantee disputes.

For a Florida physician, the malpractice exposure is structural. Florida has oscillated on non-economic damage caps, and the uncertainty itself is a planning problem — you cannot design around a cap that may not exist when the verdict comes in.

For a Florida real estate developer or investor, the exposure comes from personal guarantees on recourse carve-outs, construction financing, and bridge debt. A project that goes sideways can produce a judgment that reaches everything outside a properly structured entity stack.

And for every Florida HNW individual, there is a threat category most advisors never discuss — family law creditors. Under Bacardi v. White and Berlinger v. Casselberry, alimony and child support claimants can penetrate even discretionary and spendthrift trusts through continuing garnishment of distributions. This is a Florida-specific vulnerability that affects estate planning decisions at every wealth level.

The domestic exemptions give Florida residents a false floor. They are real protections — but they are not a complete answer.

What Olmstead Did to Florida LLC Planning

If you have a single-member LLC holding Florida assets, you need to understand what happened in 2010 and what the Florida legislature did about it.

In Olmstead v. FTC, the Florida Supreme Court held that a charging order was not the exclusive remedy against a debtor’s interest in a single-member LLC. The court allowed the creditor to obtain an order compelling the debtor to surrender all right, title, and interest in the entity — effectively permitting foreclosure on the entire membership interest rather than limiting the creditor to a lien on future distributions.

The Florida legislature responded. But not in the way most people assume.

Under Florida Statutes Section 605.0503, multi-member LLCs with truly independent members and non-illusory economics receive charging order exclusivity — the creditor is limited to intercepting distributions and cannot foreclose the interest or step into management.

But Section 605.0503(4) codified Olmstead for single-member LLCs. If a creditor can show that distributions under a charging order will not satisfy the judgment within a reasonable time, the court may order foreclosure on the entire SMLLC interest — converting a passive lien into full ownership and control.

The legislature did not reverse Olmstead. It ratified it.

This means that a single-member LLC holding your Florida real estate, your practice, or your investment account is not an asset protection structure. It is an organizational tool with a creditor vulnerability most Florida attorneys are not telling their clients about.

The fix is not moving to a different state for your LLC. The fix is proper layering — which is exactly what the Dynasty Bridge Trust™ is designed to provide.

The Estate Tax Problem Florida Residents Are Not Running the Numbers On

Florida’s lack of a state estate tax is real. It is also the source of a planning blind spot that costs Florida families tens of millions of dollars across generations.

Here is the math.

The federal estate and gift tax exemption is currently $15 million per individual — $30 million per married couple — set permanently under current law at a 40% rate above that threshold. Florida residents focus on this number and conclude they are in good shape.

But the relevant question is not where your estate is today. It is where your estate will be in 20 or 30 years.

A physician in Miami or Tampa with a $12 million net worth at age 55 — practice equity, qualified plans, brokerage accounts, real estate — is growing that estate at a compounding rate. Florida real estate alone, appreciating at 5% annually, doubles in roughly 14 years. A $4 million real estate portfolio today becomes $8 million in 14 years and $13 million in 25 years — on that single asset class.

Add portfolio growth, practice value appreciation, and continued savings, and the same physician who is “under the exemption” today is looking at a $25 million to $40 million estate by the time their children are inheriting.

At that point, the federal estate tax is 40 cents on every dollar above the exemption. No negotiation. No appeal.

And then it compounds across generations.

A married Florida couple with a $15 million estate today. Generation two inherits it, it grows at 6% over 25 years — that is $64 million. After the exemption, roughly $49 million is exposed. At 40%, that is a $19.6 million loss at the first generational transfer. Generation three receives $44 million, grows it another 25 years — now you are looking at $190 million. After exemption, $175 million is taxable. Another $70 million gone.

Total extracted across two generational transfers on a $15 million Florida starting point: approximately $89 million.

That is not a tax rate. That is a family tax. And it compounds against every Florida family that does nothing.

Florida Has No DAPT Statute — And That Matters

Florida is one of the states that explicitly does not recognize domestic asset protection trusts.

Under Florida Statutes Section 736.0505, a settlor’s creditors may reach the assets of a trust created by the settlor for his or her own benefit. Florida courts have applied this provision to self-settled trusts regardless of what the trust instrument says about spendthrift protection.

This is not a gap in the law. It is a deliberate policy choice — and Florida courts enforce it.

What this means practically: a Florida resident who establishes a self-settled irrevocable trust in Florida, hoping to retain beneficial interest while excluding creditors, gets no protection. The trust is reachable.

Nevada, South Dakota, and Delaware expressly authorize self-settled spendthrift trusts. Florida does not. And Florida courts have shown willingness to apply Florida’s public policy even when the trust is governed by a more favorable state’s law — particularly when the settlor remains a Florida resident and the dispute is litigated in a Florida court.

This makes the offshore jurisdictional layer of the Bridge Trust® structure even more important for Florida residents than for clients in DAPT-friendly states. The Cook Islands enforcement mechanism does not depend on Florida recognizing self-settled spendthrift protection — it operates through a foreign law framework that Florida courts cannot simply override.

The Four-Layer Answer for Florida

The Dynasty Bridge Trust™ is built from the ground up — and for Florida residents, each layer addresses a specific vulnerability in the Florida legal environment.

Layer one is the LLCs. State-matched entities holding the risky assets — a Florida professional entity for the medical practice, a Florida LLC for the rental properties, structured with multiple members to preserve charging order exclusivity under Section 605.0503(2). The job of the LLC is compartmentalization. It is a necessary first layer. Given Olmstead and its codification, it is never a sufficient last layer.

Layer two is the Arizona Multi-Member Limited Partnership. The LLCs flow up into the AMLP, which owns their membership interests. Arizona Revised Statutes Section 29-3503 provides charging order exclusivity for multi-member entities — and Arizona courts have consistently enforced it. The NextGear Capital v. Owens decision in 2023 reaffirmed that a charging order is the exclusive remedy. A creditor gets the right to wait for a distribution that will never come. They cannot force a sale, step into management, or compel a distribution. The partnership structure also provides constitutionally protected property rights that go beyond what a charging order alone delivers — a distinction that matters in aggressive collection environments like Florida.

Layer three is the Bridge Trust® — and this is where the Florida-specific DAPT gap is directly addressed. The AMLP interest is held inside the Bridge Trust®, which operates as a domestic grantor trust under IRC Sections 671 through 677 for tax purposes. No change to your return. No FBAR exposure in the baseline structure. But the governing instrument contains a foreign enforcement mechanism — the Emergency Override Declaration under Sections 51 through 54 — that shifts enforcement jurisdiction to the Cook Islands without a court order if a creditor moves to execute against trust assets.

Cook Islands law does not recognize Florida judgments. It does not recognize any foreign court judgment. It imposes a fraud burden of proof beyond reasonable doubt, strict limitation periods, and a bond requirement of approximately $50,000 just to initiate a claim — with fee-shifting if the creditor loses. This structure has withstood over 300 court challenges across 30-plus years. None have successfully reached the assets through that offshore layer.

For Florida residents specifically — where Section 736.0505 would allow creditors to reach a self-settled domestic trust — the offshore enforcement layer is the gap-filler that no Florida-based structure can provide.

Layer four is the Dynasty Trust. Downstream of the Bridge Trust® sits the generational planning layer. Once you pass, the Bridge Trust converts into a Dynasty Trust.

For Florida residents, a dynasty trust is accessible and effective when properly structured — Florida courts are far more likely to respect a dynasty trust where the settlor is not also a beneficiary than a self-settled DAPT arrangement.

Assets inside this structure do not pass through your taxable estate. They do not pass through your children’s estates. They do not pass through your grandchildren’s estates. The 40% federal estate tax is not triggered because the taxable transfer event never occurs. The $89 million generational erosion problem described above — solved.

And the spendthrift protection extends to your beneficiaries. If your child faces a divorce, a judgment, or a bankruptcy, the inheritance inside the Dynasty Trust is protected from their creditors. What you built does not become exposed through their life circumstances.

The Florida Opportunity Right Now

The window that matters is the one you cannot recover. Every year a Florida family’s estate appreciates inside an unprotected structure, that appreciation compounds inside the taxable estate rather than inside the protected vehicle. That lost positioning cannot be reversed. It cannot be allocated after the fact. The GST exemption, once used, cannot be reclaimed if Congress changes the law — but the allocation you lock in today is protected under Treasury Regulation Section 20.2010-1(c) regardless of future legislative changes.

The Question That Actually Matters

Most Florida families at $15 million or more have a revocable living trust, one or more LLCs, and a standard A/B structure. They have been told they are in good shape.

For probate — they are.

For a determined plaintiff attorney with discovery tools and a Florida court willing to apply Olmstead — they are not.

And for the generational estate tax problem compounding at 6% annually over the next 25 to 50 years — they are not.

The Dynasty Bridge Trust™ does not ask you to choose between solving the creditor problem and solving the legacy problem. It solves both. Simultaneously. Inside one integrated structure built from the ground up.

The Step-Up in Basis Advantage Traditional Dynasty Trusts Forfeit

The Dynasty Bridge Trust™ captures a tax benefit that traditional dynasty planning eliminates entirely. The mechanism is the step-up in basis at death under IRC § 1014, and the math difference between the two approaches is large enough to fundamentally alter the after-tax result for the next generation.

Under IRC § 1014, when an asset that is part of the decedent’s gross estate at death passes to heirs, its cost basis resets from the original purchase price to fair market value as of the date of death. A founder who purchased $200,000 of company stock that grew to $8 million during her lifetime — holding it inside a structure that keeps the asset in her estate — dies with that stock at an $8 million basis. Her heirs can sell that stock the next day and pay zero federal capital gains tax. The $7.8 million of appreciation that accrued during her life is wiped clean.

A traditional dynasty trust forfeits this benefit entirely. When assets are transferred into a traditional dynasty trust, the transfer is treated as a completed gift. The assets are removed from the grantor’s estate at funding. Because they are not in the estate at death, IRC § 1014 does not apply. The heirs inherit the original cost basis — $200,000 in the example above — and pay capital gains tax on the full $7.8 million of appreciation when the assets are eventually sold. At combined federal and state rates that often exceed 30%, that produces more than $2.3 million of capital gains liability that the Dynasty Bridge Trust™ structure eliminates by design.

The reason the Dynasty Bridge Trust™ captures the step-up is the same reason it provides creditor protection during your lifetime: the Bridge Trust® component operates as a U.S. domestic grantor trust during the settlor’s life, classified under IRC §§ 671–677 and § 7701. Assets held inside the trust are treated as owned by the grantor for income tax and estate tax purposes. They are part of the grantor’s estate. They qualify for the step-up at death.

A traditional dynasty trust must give up grantor trust status — and the estate inclusion that comes with it — in order to remove assets from the estate for transfer tax purposes. The Dynasty Bridge Trust™ does not face this trade-off because it is designed to use both treatments at the right time. During the settlor’s life, the trust is in the estate, the grantor has full access, the step-up is preserved, and the Cook Islands jurisdictional barrier defends against creditor claims. At the death of the second spouse, the step-up is captured under § 1014, the GST exemption is allocated to the converted trust at that time, and the trust transitions into its dynasty phase to hold and compound family wealth across generations without estate tax triggered at each transfer.

For families below the federal estate tax exemption — currently $15 million per individual, $30 million per couple — this is the structural advantage that defines the choice. The estate tax exemption fully shelters the assets from federal estate tax. The grantor trust status preserves the step-up at death. The dynasty conversion at second death extends the wealth multi-generationally without erosion at each transfer. All three benefits accrue simultaneously, by design, in a single integrated structure.

The advisor who recommends a traditional dynasty trust to a family below the exemption is recommending the elimination of a significant tax benefit in exchange for transfer tax planning that the exemption alone already accomplishes.

If you are a Florida physician, developer, business owner, or executive with $15 million or more in exposed assets and you want to understand what your current structure actually protects — that is the conversation to have.

Structure before stress.

For a confidential legal consultation with an Asset Protection Attorney, contact Bradley Legal Corp. at (888) 773-9399 or visit btblegal.com.