A real estate developer in his mid-fifties called me from his Phoenix office with what he described as a planning problem his estate attorney would not directly address. He and his wife — a partner at a regional consulting firm — had funded paired Spousal Lifetime Access Trusts in 2024, before the One Big Beautiful Bill Act made the federal estate tax exemption permanent at $15 million per individual.

Their combined net worth at the time was approximately $13 million. Their advisor had explained that the exemption was scheduled to sunset at the end of 2025, which would have cut it roughly in half. The SLATs would lock in the higher exemption while it was still available. Each spouse funded a SLAT with $5 million for the benefit of the other spouse and the children. The advisor framed the planning as urgent and time-sensitive — it needed to happen before the sunset, or the family would lose the opportunity permanently.

The OBBBA was signed into law on July 4, 2025. The federal estate and gift tax exemption was made permanent at $15 million per individual and $30 million per married couple. The sunset that justified the urgency never happened.

The developer was now sitting with $10 million in two separate irrevocable trusts he could not dissolve, that did not actually solve any estate tax problem because his $13 million estate had always been below the doubled exemption, that exposed the assets to his wife’s creditors and any future divorce risk, and that had forfeited the step-up in basis on the appreciated commercial property and business interests inside them. The “indirect access” his advisor had described as the SLAT’s central feature was not actually functional — distributions required his wife’s separate trustee to act, and any meaningful drawdown raised reciprocal trust doctrine concerns.

He had one question: “What were we actually solving for?”

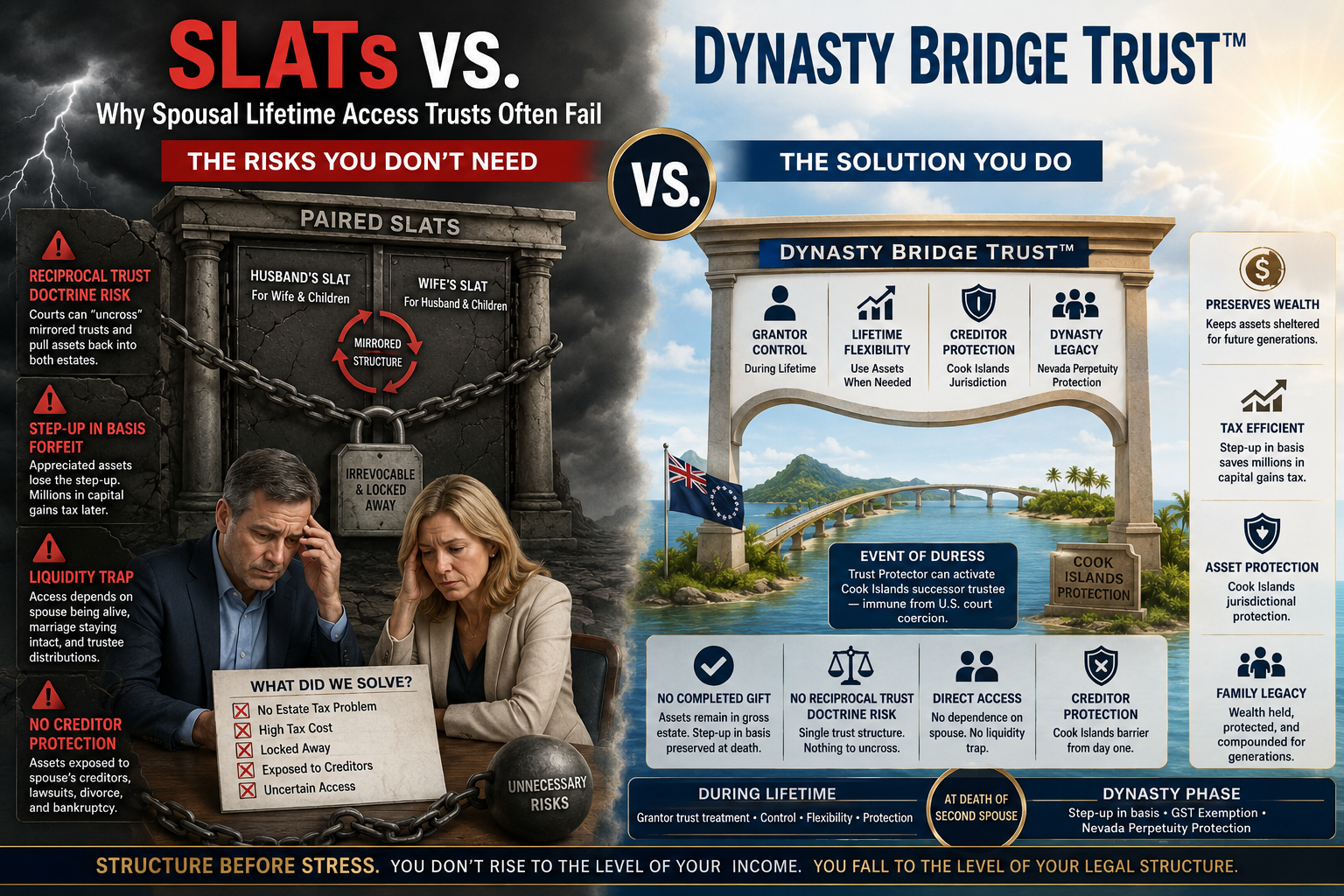

The answer to that question is what this article is about. The SLAT is a sophisticated estate planning tool with a real and legitimate use case. But it is being pitched aggressively to families who do not face the problem the SLAT is designed to solve, with downside risks the advisors who pitch it rarely disclose. For most $12 million to $30 million families, the SLAT is not the right answer. The Dynasty Bridge Trust™ is.

⸻

What a Spousal Lifetime Access Trust Actually Is

A Spousal Lifetime Access Trust is an irrevocable trust funded through a completed gift, in which the grantor’s spouse and typically their descendants are the beneficiaries. The grantor transfers assets into the trust. The transfer is treated as a permanent gift for federal transfer tax purposes. Federal lifetime gift tax exemption equal to the value of the gift is consumed at funding.

The structural feature that distinguishes the SLAT from a traditional Dynasty Trust is the inclusion of the grantor’s spouse as a beneficiary. The intent is that the grantor, while not directly accessing trust assets, retains a kind of indirect access through distributions made to the spouse during the marriage. If the grantor needs liquidity, the theory goes, the trustee can distribute to the spouse, who can then use the funds in a manner that benefits the household.

The SLAT is typically pitched as the answer to a real tension in estate planning. Traditional Dynasty Trusts remove assets from the estate but do not allow the grantor any continuing access. For families who want to use lifetime exemption against future estate tax exposure but are uncomfortable losing access entirely, the SLAT presents itself as a middle-ground solution.

The most common implementation is the paired SLAT — husband establishes a SLAT for the benefit of the wife and children; wife establishes a SLAT for the benefit of the husband and children. Both trusts have identical or near-identical terms. The intent is for each spouse to retain indirect access to the other spouse’s trust during the marriage, while both trusts fully utilize lifetime exemption against the couple’s combined estate tax exposure.

This paired structure is exactly where most SLATs fail.

⸻

The OBBBA Exemption Reality

Many SLATs funded between 2020 and 2025 were pitched on a specific timing argument. The federal estate tax exemption was scheduled to sunset at the end of 2025, reducing it from approximately $14 million per individual to roughly half that amount. Advisors framed SLATs as urgent action items — fund them before the sunset, or lose access to the higher exemption forever.

The One Big Beautiful Bill Act, signed into law on July 4, 2025, made the federal estate and gift tax exemption permanent at $15 million per individual and $30 million per married couple. The sunset urgency that drove much of the 2024-2025 SLAT funding wave is gone. The exemption is high. The exemption is permanent. And the exemption alone fully shelters the vast majority of families who funded SLATs during that period.

For a $13 million couple, the federal estate tax exposure is zero. The $30 million combined exemption sits well above the estate value. Removing assets from the estate at funding accomplishes nothing in terms of federal estate tax planning, because there was no federal estate tax to plan against in the first place.

A handful of states impose their own estate taxes with lower exemptions, and state exposure should be addressed where it exists. But for the broad majority of $12 million to $30 million families in non-estate-tax states, the SLAT is solving for an estate tax problem that does not exist. The structure is solving for a phantom liability while introducing real ones.

⸻

The Reciprocal Trust Doctrine Trap

The most aggressive failure mode for paired SLATs is the reciprocal trust doctrine, established by the Supreme Court in United States v. Estate of Grace, 395 U.S. 316 (1969). The doctrine permits courts to “uncross” mirrored trust structures and treat the assets as if each grantor had funded a trust for their own benefit, eliminating the gift treatment and pulling the assets back into the gross estates of both grantors.

The policy underlying the doctrine is straightforward. If two spouses execute substantially identical trusts naming each other as beneficiaries, the practical economic position of each spouse before and after funding is unchanged. Each spouse continues to enjoy access to the same pool of family assets. The only thing that has changed is the formal title — and form alone is insufficient to support the favorable transfer tax treatment that completed gift status confers.

Under Estate of Grace, courts apply a substance-over-form analysis. If the two trusts leave each grantor in approximately the economic position they would have occupied without the trusts, the doctrine collapses the gift treatment. The assets are returned to the grantors’ gross estates. Any lifetime exemption used at funding is restored, and the SLAT structure delivers nothing of what it was designed to deliver.

To survive the doctrine, mirrored SLATs must establish meaningful differentiation. Different funding amounts. Different timing — typically separated by months, not days. Different beneficiary classes. Different distribution standards. Different trustees. Different funding sources. The drafting standard is high, and the burden of proof rests on the taxpayer if the IRS challenges the structure.

Most paired SLATs pitched to $12 million to $30 million families do not meet this standard. They are drafted from templates. Both trusts use the same boilerplate language. Both are funded close in time. Both have identical beneficiary classes and distribution standards. Under modern doctrine application, these structures are increasingly vulnerable.

The risk is asymmetric. The taxpayer cannot compel the IRS to accept the SLATs as separate trusts. The IRS can challenge the structure at any time during the statute of limitations on the gift tax return. And if the doctrine is applied, the planning collapses retroactively — the assets are pulled back into both estates, the lifetime exemption is restored as if the gifts had never been made, and the family is left with the same estate tax exposure they had before, plus the legal fees of defending the failed structure.

⸻

The Step-Up in Basis Forfeit

Even when a SLAT survives reciprocal trust doctrine scrutiny, it imposes the same step-up in basis forfeit that traditional Dynasty Trusts impose. The completed gift at funding removes the assets from both spouses’ gross estates. IRC § 1014 — which provides a stepped-up basis to fair market value at death for assets in the decedent’s gross estate — does not apply.

The practical consequence is that appreciated assets transferred into a SLAT take carryover basis from the original cost basis at funding. When the trust eventually sells those assets, federal capital gains tax is owed on the full lifetime appreciation. For founders, executives, real estate investors, and any other clients holding low-basis appreciated assets, the capital gains tax owed by the SLAT on the eventual sale can run into the millions of dollars per family.

For families below the federal exemption — where there was no estate tax problem to solve in the first place — this capital gains tax cost is paid for nothing. The transfer tax planning the SLAT was supposed to deliver is irrelevant because the exemption already covered the estate. The capital gains tax is the price of solving a problem that did not exist.

The math is fully developed in our companion article on dynasty trust step-up forfeit, which applies to SLATs in the same way it applies to traditional Dynasty Trusts. The step-up forfeit alone disqualifies the SLAT for most $12 million to $30 million families, before the additional failure modes are even considered.

⸻

The Liquidity Trap

The “indirect access” mechanism that makes SLATs attractive is the structure’s most fragile component. The grantor does not have direct access to SLAT assets. Access flows only through the beneficiary spouse, in the form of distributions the trustee makes to that spouse during the marriage. For the indirect-access path to function, three conditions must be continuously satisfied: the marriage must remain intact, the beneficiary spouse must be alive, and the beneficiary spouse must direct or permit the trustee to make distributions that benefit the household.

Each of these conditions can fail unpredictably. If the beneficiary spouse predeceases the grantor, the access path closes. The trust continues for the children, but the surviving grantor has no remaining mechanism to access the assets indirectly. If the spouses divorce, the access path closes for the same structural reason — the former spouse has no ongoing obligation, and typically no ongoing inclination, to facilitate distributions that benefit the grantor. If the beneficiary spouse simply makes independent decisions about distributions during the marriage, the access path was never reliable in the first place.

The probability of at least one of these scenarios materializing across a thirty- or forty-year planning horizon is meaningful. Couples in their early sixties at the time of funding face the actuarial reality that one spouse is statistically likely to predecease the other by a significant margin. The “access” the SLAT promises is contingent on circumstances that frequently change over the relevant time horizon.

For families relying on the indirect-access path as a planning safety net, the SLAT delivers a planning fiction. The access either works perfectly or fails completely, and there is no middle ground.

⸻

No Creditor Protection

A SLAT addresses estate tax exposure. It does not address creditor exposure. The trust assets are reachable by anyone with a legitimate claim against the beneficiary spouse — creditors of the beneficiary spouse’s business activities, judgment creditors from any litigation against the beneficiary spouse, divorcing spouses, and bankruptcy trustees if the beneficiary spouse files for protection.

The exposure is not theoretical. The same indirect-access mechanism that the SLAT uses to deliver liquidity to the household is the mechanism that exposes the trust assets to anyone with a claim against the beneficiary spouse. If the trustee distributes to the spouse, those distributed funds become reachable. If the trust holds business interests or income-producing real estate, the income flowing to the spouse is reachable. The structure is designed to create a flow of value from the trust to the beneficiary spouse, and any creditor of that spouse stands ready to attach the flow.

For physicians, real estate investors, business owners, and other high-liability professionals — exactly the demographic SLATs are most often pitched to — the SLAT introduces no creditor protection at all. If anything, it can amplify exposure by routing assets through the higher-liability spouse’s beneficial interest.

The Dynasty Bridge Trust™, by contrast, delivers Cook Islands jurisdictional creditor protection from the moment of funding. The grantor’s lifetime creditor exposure is addressed structurally, not left as an open vulnerability the SLAT does not even attempt to solve.

⸻

The Dynasty Bridge Trust™ Alternative

The Dynasty Bridge Trust™ is structured to deliver every benefit a SLAT promises, without any of the failure modes a SLAT introduces.

There is no completed gift at funding. The trust qualifies as a U.S. domestic grantor trust under IRC §§ 671 through 677 and § 7701, with the grantor treated as the owner of the trust assets for federal income tax and estate tax purposes during the grantor’s lifetime. Lifetime exemption is preserved. The assets remain in the grantor’s gross estate, which is exactly where they need to be to qualify for the IRC § 1014 step-up at death.

There is no reciprocal trust doctrine risk. The Dynasty Bridge Trust™ operates as a single integrated trust, not as a mirrored pair. There is no second trust to uncross. The doctrine has no purchase against the structure.

There is no liquidity trap. The grantor retains operational control of the trust during life and may receive distributions directly under the grantor trust framework. There is no dependence on a beneficiary spouse to facilitate access. The marriage’s stability and the spouse’s lifespan have no bearing on the grantor’s ability to use the trust assets.

There is no creditor exposure to the beneficiary spouse’s claims, because the structure does not depend on routing assets through the spouse. The Bridge Trust® component delivers Cook Islands jurisdictional protection — a creditor enforcement barrier that no domestic structure provides — from the moment of funding. At a credible threat, the Trust Protector may declare an Event of Duress, transitioning administration to the pre-designated Cook Islands successor trustee, who is statutorily prohibited from complying with U.S. court coercion.

At the death of the second spouse, the trust converts into its dynasty phase. The IRC § 1014 step-up is captured. The GST exemption is allocated to the converted dynasty trust at that time. The dynasty phase continues under Nevada law, which has eliminated the Rule Against Perpetuities, holding and compounding family wealth across generations without estate tax triggered at each transfer.

The SLAT solves one problem partially while introducing four problems entirely. The Dynasty Bridge Trust™ solves all of them in a single integrated structure.

⸻

When a SLAT Actually Makes Sense

The SLAT is not a wrong tool. It is a tool designed for a specific situation, and within that situation, it can be deployed effectively.

That situation is families with combined net worth meaningfully above the federal estate tax exemption — typically $40 million and up — where actual transfer tax exposure to the 40% federal estate tax rate is large, where lifetime exemption use is justified by the size of the estate, and where the family is willing to accept the step-up forfeit, the reciprocal trust doctrine risk, the liquidity trap, and the absence of creditor protection because the estate tax savings outweigh those costs in absolute terms.

Even for above-exemption families, sophisticated planning rarely uses paired SLATs alone. Multi-tool architectures often combine a single SLAT with a Dynasty Bridge Trust™, charitable lead trusts, intentionally defective grantor trusts, or other structures, each carrying a portion of the planning burden according to the specific tax exposure each is designed to address.

But for the broad band of $12 million to $30 million families being advised to fund paired SLATs as general estate planning, those families are accepting structural risks for benefits they do not need.

⸻

The Decision Framework

The decision between paired SLATs and the Dynasty Bridge Trust™ for a family in the $12 million to $30 million range comes down to four questions.

First, do you have an actual federal estate tax problem? With the OBBBA-permanent $15 million individual and $30 million couple exemption, most families in this band do not.

Second, are you comfortable accepting the reciprocal trust doctrine risk? Mirrored SLATs require meaningful differentiation to survive Estate of Grace scrutiny, and most do not meet the standard.

Third, do you need creditor protection during your lifetime? The SLAT provides none. The Dynasty Bridge Trust™ provides Cook Islands jurisdictional protection from the moment of funding.

Fourth, are you comfortable with the indirect-access mechanism’s contingencies? If the beneficiary spouse predeceases or divorces, the access path closes and the assets are locked away.

For families below the federal exemption, exposed to creditor risk, holding appreciated assets, and uncomfortable with the contingencies inherent in indirect-access planning — which describes the typical $12M to $30M client — the Dynasty Bridge Trust™ is the structurally correct answer. The SLAT solves a problem these families do not face while introducing problems they did not need to accept.

⸻

Spousal Lifetime Access Trust FAQs

What is a Spousal Lifetime Access Trust?

A SLAT is an irrevocable trust funded through a completed gift, with the grantor’s spouse and typically descendants as beneficiaries. The structure is designed to remove assets from the grantor’s estate while preserving indirect access through distributions to the beneficiary spouse during the marriage.

How does the reciprocal trust doctrine apply to paired SLATs?

The reciprocal trust doctrine, established in United States v. Estate of Grace, 395 U.S. 316 (1969), permits courts to uncross substantially identical mirrored trust structures and treat the assets as if each grantor had funded a trust for their own benefit. When the doctrine applies, the gift treatment collapses, the assets are returned to both grantors’ gross estates, and the SLAT planning fails. Most paired SLATs pitched to families in the $12M to $30M range do not meet the differentiation standard required to survive doctrine scrutiny.

What happens to a SLAT if the beneficiary spouse dies first?

The trust continues for the remaining beneficiaries — typically the children — but the indirect-access path closes. The grantor has no remaining mechanism to access the trust assets. Any liquidity the grantor was relying on through the spouse’s beneficial interest is no longer available.

What happens to a SLAT in a divorce?

The trust does not automatically dissolve. The former spouse retains beneficial interest under the trust terms unless the trust includes specific divorce contingency language — and even then, the practical access path is severed. The grantor cannot recover the assets. The lifetime exemption used at funding is permanently consumed.

Can I unwind a SLAT after funding?

Generally, no. SLATs are irrevocable by design — the irrevocability is what makes the gift treatment effective. Decanting, judicial modification, or non-judicial settlement may be available in narrow circumstances, but each of these comes with potential tax consequences and litigation risk.

Does a SLAT provide creditor protection?

For the grantor, the SLAT provides only the limited protection that comes from the assets no longer being titled in the grantor’s name. The assets are reachable by creditors of the beneficiary spouse, including divorce creditors and judgment creditors. The Dynasty Bridge Trust™ provides Cook Islands jurisdictional protection that no version of a SLAT delivers.

Are SLATs still useful after the OBBBA permanent exemption?

For families below the $30 million couple exemption, the OBBBA permanence eliminates the urgency that drove much of the 2024–2025 SLAT funding wave. The exemption alone now shelters these families from federal estate tax. SLATs remain useful in narrow circumstances — typically for families well above the exemption — but for the broad band of $12M to $30M clients, the structure no longer solves a problem the family actually faces.

The Bottom Line

The Spousal Lifetime Access Trust is a sophisticated estate planning tool designed for a narrow set of circumstances. For families well above the federal estate tax exemption, with appropriate differentiation between mirrored structures and acceptance of the structural compromises, the SLAT can be deployed effectively as part of a broader multi-tool architecture.

For the broad band of $12 million to $30 million families being advised to fund paired SLATs as general estate planning, the SLAT is solving for transfer tax exposure these families do not face, while introducing structural risks they did not need to accept. The reciprocal trust doctrine threatens the gift treatment. The step-up forfeit imposes a multi-million-dollar capital gains cost. The liquidity trap closes the moment the beneficiary spouse predeceases or divorces. And the absence of creditor protection leaves the grantor exposed to the very lawsuits and judgments most HNW clients are most concerned about.

The Dynasty Bridge Trust™ delivers every benefit the SLAT promises — multi-generational wealth protection, lifetime planning flexibility, integration with the family’s broader estate planning — without any of the failure modes. It is the structurally correct answer for most $12 million to $30 million families.

If your estate planning advisor has recommended a SLAT or a paired SLAT structure, ask the four questions above. If the answers do not satisfy you, the Dynasty Bridge Trust™ is the alternative most advisors do not know to offer.

Structure before stress. You don’t rise to the level of your income. You fall to the level of your legal structure.

📞 For a confidential legal consultation with an Asset Protection Attorney, contact Bradley Legal Corp. at (888) 773-9399 or visit btblegal.com.

By: Brian T. Bradley, Esq.

National Asset Protection Attorney | Bradley Legal Corp.