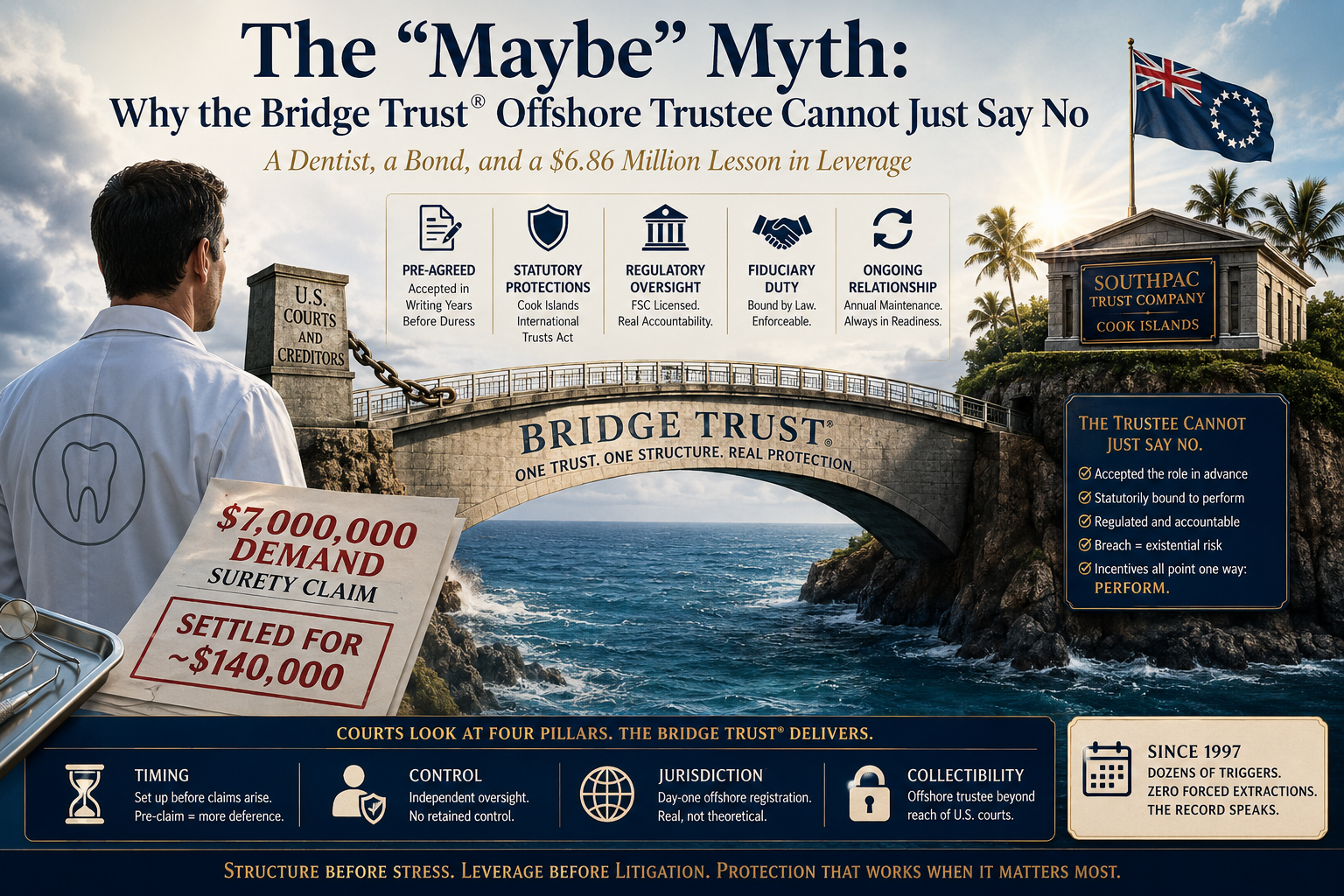

A Dentist, a Bond, and a $6.86 Million Lesson in Leverage

In 2007, a dentist with roughly $5–6 million in assets co-signed a construction performance bond for his brother, a builder taking on his first large project. The brother could not qualify on his own. Then 2008 happened. The project froze mid-build. The surety came for the brother first and found nothing. Then it came for the dentist on a $7 million demand.

What happened next is the point of this article. Before any of this, the dentist had completed a full asset protection structure including a Bridge Trust®. By the time the surety was at the door, every dollar of meaningful exposure was already inside a properly funded, properly registered, properly maintained structure. The Trust was never triggered. It did not need to be.

What is The Bridge Trust®?

The $7 million claim settled for approximately $140,000.

That is what leverage looks like in real-world asset protection. And it is the exact outcome a particular line of criticism — circulating among commentators selling competing structures — claims is impossible because, they argue, “there is no guarantee the offshore trustee will actually step in.”

The premise of that critique is wrong, but not for the reasons most defenders of the Bridge Trust® articulate. This article explains why — accurately.

The Attack, Stated Fairly

The critique runs roughly like this:

“The Bridge Trust® depends on an offshore Cook Islands trustee to step in once an event of duress has been declared. But no trustee has publicly committed to do so under all circumstances. They can simply refuse. There is no guarantee the structure will actually trigger. You are banking on a maybe.”

It is a clean, emotionally effective argument. It plays on the layperson’s instinct that anything involving offshore parties must be uncertain.

The argument has two fatal problems. It misframes how licensed offshore trustees actually operate. And when the critic is selling a fully foreign Cook Islands trust as the alternative — which is the most common case — the same critique applies with equal force to the critic’s own product.

The Pre-Agreement Reality

The Special Successor Trustee in a Bridge Trust® is not a trustee being solicited for the first time at the moment of duress. The trustee is identified by name in the trust agreement itself, signs as a party to the instrument at formation, and performs initial know-your-customer (KYC), due diligence (DD) work on the client before any signature is given. The SST has been pre-vetted. That pre-engagement framework is structural and creates meaningful operational advantages over crisis-time trustee solicitation.

What pre-engagement does not do is eliminate the trustee’s independent fiduciary discretion at the moment of acceptance. Every licensed offshore trustee — in every jurisdiction in the world — must confirm at trigger that accepting the role remains consistent with its statutory, licensing, and fiduciary obligations against current circumstances. That confirmation is a fitness review, not a re-litigation of whether to participate in the structure at all.

The distinction matters. A trustee performing a fitness review against current facts is in a fundamentally different posture than a trustee being approached cold during active litigation. The first is confirming the engagement remains operable. The second is being asked to accept an engagement that has never existed.

In a properly structured Bridge Trust® with clean facts — pre-claim funding, no intervening criminal exposure, complete due diligence on all contributing parties, no pre-existing court orders affecting trust assets — the trigger-stage fitness review is a confirmation rather than a new decision.

What anchors the trustee’s commitment is not an ongoing fee relationship. It is:

• The signed trust instrument identifying the trustee as a party to the agreement

• Licensing obligations under the Cook Islands Financial Supervisory Commission

• The Cook Islands Trustee Companies Act 1981–82, governing the conduct of trust companies operating in the jurisdiction

• The Cook Islands International Trusts Act 1984 (as amended), which directs Cook Islands trustees to disregard foreign court orders that would harm the beneficiary and prohibits the trustee from honoring U.S. judgments

• Common law fiduciary principles enforceable against the trustee by the beneficiaries

A licensed Cook Islands trustee that arbitrarily refused to honor a properly accepted role would face breach of fiduciary duty claims, regulatory enforcement, and license consequences. The economic and regulatory framework points toward performance — but only where the underlying facts permit performance consistent with the trustee’s other obligations.

When the Trustee Can — and Will — Decline

To be precise about what licensed offshore trustees can and cannot do:

A licensed Cook Islands trustee will decline to accept a trusteeship at trigger when accepting would put the trustee in independent regulatory or fiduciary breach. Examples include:

• The client has become subject to criminal proceedings or sanctions that implicate the trust assets

• The trust assets are reasonably suspected to represent proceeds of crime

• The trust assets are already subject to a court injunction that prevents retitling into the offshore trustee’s name at the time of trigger

• A contributing party other than the grantor cannot or will not provide updated due diligence required for the trustee to verify the source of contributed assets

These are not arbitrary refusals. They are the same fiduciary and licensing constraints every regulated trust company in every jurisdiction operates under. No competent practitioner would argue otherwise. The distinction worth holding is between (a) a licensed trustee performing legitimate fitness review and (b) the critique’s implied claim that offshore trustees casually decide at the last moment whether they want involvement. Those are entirely different concepts.

What Critics of the Bridge Trust® Get Wrong!

The relevant question for sophisticated planning is whether the structure is built such that, when triggered against clean facts, the trustee acceptance review functions as a confirmation rather than a re-evaluation. A properly structured Bridge Trust® — fully funded pre-claim, with timing and control discipline maintained throughout, with due diligence completed on all contributing parties at formation — produces that result. A defective structure does not. The critique’s force depends on conflating the second with the first.

The Glass House: When the “Maybe” Critique Describes the Critic’s Own Product

The most common attack on the Bridge Trust® does not come from domestic-only practitioners. It comes from sellers of fully foreign Cook Islands trusts who position their product as the “real” asset protection answer and the Bridge Trust® as a watered-down imitation that depends on a “maybe.”

That argument is structurally incoherent.

A fully foreign Cook Islands asset protection trust requires every single one of the following:

• Day-one offshore registration in the Cook Islands

• A pre-engaged offshore trustee licensed under the Cook Islands Financial Supervisory Commission

• The same fiduciary discretion to refuse actions inconsistent with the trustee’s licensing obligations

• Reliance on the same Cook Islands International Trusts Act framework that directs trustees to disregard foreign court orders harming beneficiaries

• A duress or distress provision empowering the trustee to refuse foreign court orders

The fully foreign alternative depends on the same trustee discretion the critic attacks when used by the Bridge Trust®. If the trustee’s right to perform a fitness review at the moment of action constitutes a “maybe” when used by the Bridge Trust® platform, it is the same “maybe” when retained by the critic’s platform. The mechanism doesn’t change based on who hires it.

The fully foreign alternative depends on exactly the same mechanism the critic attacks when used by the Bridge Trust®. If a pre-engaged Cook Islands trustee under FSC oversight is a “maybe” when retained by the Bridge Trust® platform, it is the same “maybe” when retained by the critic’s platform, it is the same “maybe” when retained by the critic’s platform. The mechanism doesn’t change based on who hires it.

There are only two ways to reconcile this:

1. Licensed Cook Islands trustees reliably perform when retained against clean facts — in which case the Bridge Trust® framework works as designed, and the “maybe” critique collapses for both structures.

2. Licensed Cook Islands trustees frequently refuse engagement at the moment of action — in which case the critic’s own fully foreign product faces the same exposure and the entire offshore trust industry is built on the same supposed defect.

The critic cannot have it both ways.

Doug Lodmell of Lodmell & Lodmell has long acknowledged that a fully foreign Cook Islands trust is, in pure asset protection terms, structurally excellent. The Bridge Trust® is not designed to claim superior raw protection. It is designed to deliver substantially equivalent protection — through the same statutory framework, the same pre-engaged trustee mechanism, the same offshore registration — while preserving domestic grantor trust tax treatment under IRC §7701(a)(30)(E) during the pre-trigger period. That means, during the quiet period the trust spends in normal operation: no Form 3520 or 3520A reporting burden, no 35% penalty exposure for late or incomplete foreign trust filings, step-up in basis at death preserved, and simple grantor trust tax administration under IRC §§ 671, 673–677.

The fully foreign alternative carries those compliance burdens from day one in exchange for marginal additional protection the Bridge Trust® already supplies through the same offshore infrastructure. The critic’s framing — “we’re the real one, the Bridge Trust® is a maybe” — only works if the audience never asks what the critic’s own structure depends on.

It depends on the same thing.

One Trust, Not Two: Why There Is No Transfer at Trigger

A related attack worth dispatching: the claim that triggering the Bridge Trust® constitutes a fraudulent transfer because assets supposedly “move” from a domestic trust to a foreign trust at the moment of duress

This argument also assumes a structure that does not exist.

The Bridge Trust® is one trust, not two. It is initially registered offshore, classified as a domestic grantor trust for U.S. tax purposes under the two-part test of IRC §7701(a)(30)(E), and recognized in its offshore jurisdiction as of the original registration date — regardless of when an event of duress is later declared.

When duress is declared, no new trust is created. No assets are transferred from one entity to another. No decanting occurs. No conveyance event takes place. What changes is control. Authority over the existing single trust shifts from the U.S.-side control structure to the pre-engaged offshore trustee. The offshore registration has been live since day one. The trust does not become a foreign trust at trigger; it was already registered offshore. It simply ceases to qualify as a domestic trust for U.S. tax purposes.

There is no fraudulent transfer moment at trigger because there is no transfer. The transfer happened at the front end, when the trust was initially funded — and that funding is when fraudulent transfer analysis applies. If the funding occurred before any creditor claim arose, the structure satisfies the timing pillar and is not vulnerable to fraudulent transfer attack on the trigger event itself.

What Courts Actually Look For — And What the Track Record Shows

Courts evaluating asset protection structures are not impressed by labels. They look at substance, and the analysis tracks directly onto the four pillars of real-world asset protection:

Timing. Was the structure set up before the creditor claim arose? Pre-claim structures receive substantially more deference than post-claim transfers, which face fraudulent transfer scrutiny under the Uniform Voidable Transactions Act or equivalent state law.

Control. Has the settlor retained de facto control such that the trust is a sham? In a Bridge Trust®, the Trust Protector mechanism and the pre-engaged Special Successor Trustee provide independent oversight a court can review and accept.

Jurisdiction. Is the structure actually subject to the jurisdiction claimed, or is it a paper exercise? Day-one offshore registration with a licensed Cook Islands trustee under FSC oversight is real jurisdictional substance.

Collectibility. Even if a creditor obtains a judgment, can the assets actually be reached? Once authority shifts to the offshore trustee, the assets sit outside the practical reach of U.S. courts. The trustee is statutorily directed to disregard foreign court orders that would harm the beneficiary.

A properly structured Bridge Trust® satisfies all four pillars. The operational record confirms it.

The Bridge Trust® has been in continuous operation since 1997 — nearly three decades. The structure has weathered hundreds of documented pressure events. It has been activated multiple times each year. Across that period, in every Bridge Trust® matter that has reached trigger against properly maintained timing and control discipline, the Special Successor Trustee acceptance mechanism has functioned as designed. No court has succeeded in compelling forced extraction from a properly structured and triggered Bridge Trust®.

Equally important: there are no published cases adjudicating the Bridge Trust® on the merits. That is not a gap. It is the structure working at the leverage stage, not the litigation stage. Across thousands of asset protection plans implemented through this platform, the vast majority of attacks are resolved at one of four earlier hurdles — deterrence, negotiation leverage, settlement, and the stress-reduction-driven endurance to litigate without panicking — long before a triggered offshore structure has to be tested in adversarial proceedings against a final judgment creditor. The structure’s purpose is to make litigation pointless before the trigger. The leverage is the product.

The dentist did not need the trigger. The trigger was the credible threat — and that credibility came from a pre-engaged Special Successor Trustee operating under licensed offshore regulatory oversight, an offshore registration that had been live since day one, and a Trust Protector mechanism that the surety’s counsel knew would actually function if pushed.

The Domestic Alternative Fails Too

When critics push a domestic-only asset protection trust as the alternative, the analysis is even more direct. Article IV, Section 1 of the U.S. Constitution — the Full Faith and Credit Clause — requires each state to honor the judicial proceedings of every other state. A Nevada, South Dakota, Alaska, or Wyoming DAPT does not exist on an island. Its trustee is a U.S. person, subject to a U.S. court’s jurisdiction, bound by Full Faith and Credit to honor sister-state judgments.

The case law confirms the failure pattern: US vs Huckaby, Kilker v. Stillman, In re Huber, Battley v. Mortensen, and Curci Investments, LLC v. Baldwin, 14 Cal. App. 5th 214 (2017) — all instances where domestic asset protection structures collapsed against creditor process. In each case, a domestic trustee who would have preferred to refuse the creditor was structurally unable to do so. That is the actual “guarantee” being sold: a guarantee that the trustee cannot refuse.

By contrast, in FTC v. Affordable Media, LLC, 179 F.3d 1228 (9th Cir. 1999), and In re Lawrence, 279 F.3d 1294 (11th Cir. 2002), Cook Islands trustees refused to repatriate assets in response to U.S. court orders. Contempt sanctions issued against the debtors. The assets remained protected and were never recovered.

What Actually Fails – And Why

Don’t get me wrong, successor trustee mechanisms can and do fail. Not often, but it is a possibility. But the failure modes are real and worth naming directly. They fall into a small set of consistent patterns, every one of which maps onto a failure of the four pillars at the planning stage:

Timing failures. Trust assets are already subject to a court injunction or pre-existing freeze order at the time of trigger, preventing the trustee from accepting retitling into trust company control. This is a timing-pillar failure that originated long before the trigger event — the structure was not put in place far enough ahead of the creditor claim.

Control and funding failures. Trust assets were contributed by a person other than the grantor, and that contributing party cannot or will not provide updated due diligence required for the trustee to verify the source of the assets. This is a control-pillar failure at the funding stage — the structure was not built with disciplined funding from the start.

Structural defects in the underlying trust itself:

• The trust was not registered offshore at inception. The “bridge” is theoretical.

• No Special Successor Trustee was pre-engaged or pre-signed. There is nothing to trigger.

• The trust was not fully funded from day one, leaving exposed assets outside the structure.

• The Trust Protector mechanism was either absent or poorly drafted.

A trust with these defects is, in fact, banking on a maybe. It is not, however, a properly structured Bridge Trust®. And it is not a properly structured fully foreign Cook Islands trust either. Critics consistently conflate the actual Bridge Trust® with these inferior structures because that conflation is what allows the attack to gain rhetorical traction.

The honest framing is this: every offshore trust mechanism — Bridge Trust® or fully foreign — depends on disciplined structure and clean facts at the time of trigger. Where structure and facts are disciplined, the mechanism works. Where they are not, no offshore trust mechanism will save the planning. That is true universally.

Structure Before Stress

The point of asset protection planning is to put the structure in place before the stress arrives. Not because the structure produces a guaranteed outcome — no honest practitioner will use that word — but because a properly engineered, fully funded, actively maintained structure with a pre-engaged Special Successor Trustee, statutory fiduciary backing, and three decades of operational history is exactly the kind of leverage that produces favorable settlements before triggers are ever required.

The “maybe” myth assumes none of that exists. In a properly structured Bridge Trust®, all of it does — and has, demonstrably, since 1997. When the myth comes from a critic selling a fully foreign Cook Islands trust, the same supposed defect lives in the critic’s own product. The mechanism does not change based on who hires it.

Frequently Asked Questions:

1. Can the offshore trustee just say no when the Bridge Trust® is triggered?

The trustee performs a fitness review at trigger to confirm acceptance remains consistent with its statutory, licensing, and fiduciary obligations against current circumstances. In a properly structured Bridge Trust® with clean facts — pre-claim funding, no intervening criminal or sanctions exposure, complete due diligence on contributing parties at formation — that review is a confirmation rather than a re-evaluation. The trustee can decline only where independent fiduciary or licensing grounds exist (e.g. criminal proceedings against the client, suspected proceeds of crime, pre-existing court injunctions on trust assets, incomplete due diligence on non-grantor contributors). These are the same constraints every licensed offshore trustee operates under in every jurisdiction.

2. What happens if the offshore trustee refuses to perform fiduciary duties?

If decline is based on legitimate fiduciary or licensing grounds, the trustee is performing its statutory duty. The Trust Protector retains authority to appoint a successor trustee under §53.2(b) of the trust instrument. Where decline occurs, however, the underlying cause typically reflects a failure of the four pillars at the planning stage — most commonly a timing failure (pre-existing court orders) or a control and funding failure (unverifiable non-grantor contributions). The remedy for that failure lies in disciplined planning at the front end, not in any single trustee’s discretion at the back end. If the decline is not based on legitimate fiduciary or licensing grounds, the trustee faces breach of fiduciary duty claims by beneficiaries, regulatory enforcement and license revocation by the Cook Islands Financial Supervisory Commission, and loss of its operating business. The economic, legal, and regulatory incentives all push toward performance.

3. Has any properly structured Bridge Trust® ever been forced to surrender assets?

According to Doug Lodmell, who manages the platform, in nearly three decades of continuous operation since 1997 and dozens of trigger events, no court has succeeded in compelling forced extraction from a properly structured and triggered Bridge Trust®.

4. Does triggering the Bridge Trust® create a fraudulent transfer?

No. According to the firm that holds the Bridge Trust® trademark, Lodmell & Lodmell, in nearly three decades of continuous operation since 1997, across hundreds of documented pressure events with the trust activated multiple times each year, no court has succeeded in compelling forced extraction from a properly structured and triggered Bridge Trust®.

5. How does the Bridge Trust® compare to a fully foreign Cook Islands trust?

Both rely on the same offshore registration, the same pre-engaged offshore trustee mechanism, the same Cook Islands International Trusts Act framework, and the same Financial Supervisory Commission oversight. The structural protection mechanism is substantially equivalent. The difference is U.S. tax treatment during the pre-trigger period: the Bridge Trust® is classified as a domestic grantor trust under IRC §7701(a)(30)(E), avoiding Form 3520 filing requirements and 35% late filing penalty exposure during the quiet period.

6. If a critic argues the Bridge Trust® depends on a “maybe,” does that argument apply to the critic’s own fully foreign Cook Islands trust?

Yes. Any properly structured Cook Islands asset protection trust depends on the same elements: pre-engaged offshore trustee, day-one offshore registration, and reliance on the Cook Islands International Trusts Act framework. The same trustee discretion to perform a fitness review at the moment of action exists in both structures. If those elements constitute a “maybe” when assembled through the Bridge Trust® platform, they constitute the same “maybe” when assembled by anyone else.

7. Does triggering the Bridge Trust® create a fraudulent transfer?

No. The Bridge Trust® is one trust, not two. It is registered offshore from inception. At trigger, no new trust is created and no assets are transferred — control of the single existing trust shifts to the pre-engaged offshore trustee. Fraudulent transfer analysis applies to the original funding, not the trigger event.

Schedule a legal consultation with our experienced asset protection attorneys today at (888) 773-9399.

By: Brian T. Bradley, Esq.