Dr. Sarah Chen had built exactly what she set out to build.

Twelve years out of residency, she was running a successful orthopedic surgery practice in Phoenix. She owned four rental properties. She had $2.3 million in investable assets outside her retirement accounts. And she had just been named in her third malpractice claim in eighteen months — none of them with merit, all of them expensive.

Her malpractice insurer covered the defense. But the policy had limits. And Sarah had done the math. One bad jury, one runaway verdict, and everything she had built for twelve years was on the table.

She had researched her options. She knew what a Cook Islands trust could do — she understood the judgment firewall, the beyond-reasonable-doubt fraud burden, the short limitation periods. She also knew what it cost to run one. Thirty thousand dollars to set up. Twelve thousand a year in maintenance. FBAR filings. Form 3520 every year. Assets sitting in a foreign bank account she couldn’t touch without a Cook Islands trustee’s cooperation — starting immediately, whether or not she ever faced a serious threat.

She wanted the protection. She didn’t want to carry a full offshore operation indefinitely for a risk that might never materialize.

Her attorney had one more option to show her.

Quick Answer

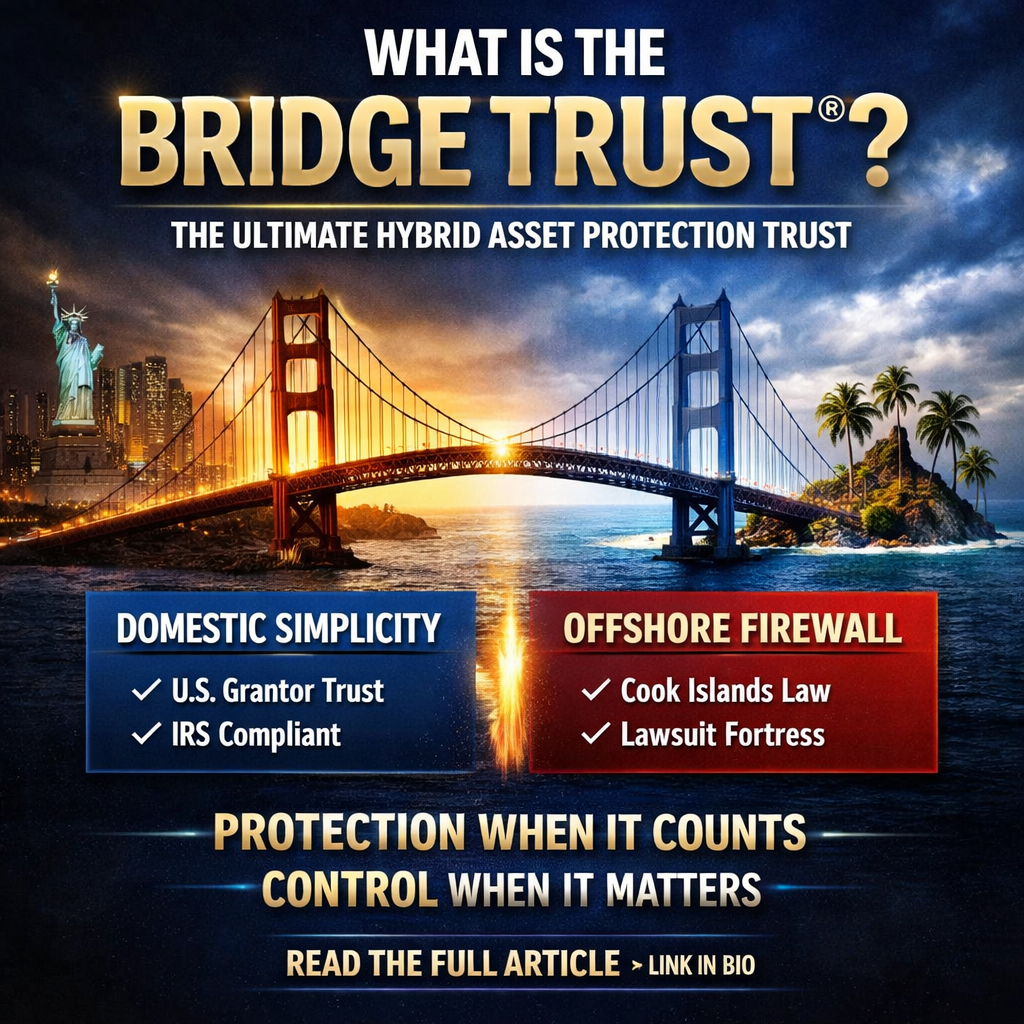

The Bridge Trust® is a hybrid asset-protection trust that operates as a U.S. grantor trust for tax purposes while being legally established under Cook Islands law from inception.

This structure allows assets to be administered domestically during normal conditions while maintaining the ability to transition offshore under independent fiduciary control if serious litigation risk arises.

It combines the simplicity of domestic administration with the jurisdictional protection of Cook Islands law — without relying on secrecy, automation, or gimmicks.

⸻

What Problem Does the Bridge Trust® Solve?

Asset protection failures almost always fall into one of two categories:

• Domestic trusts are convenient but remain fully subject to U.S. court jurisdiction.

• Fully offshore trusts are powerful but expensive and operationally complex for many families who may never face serious litigation.

The Bridge Trust® was designed to solve that exact problem.

Think of it as a hybrid engine:

• Efficient and compliant under normal conditions

• Capable of deploying maximum legal defense when real litigation risk appears

How the Bridge Trust® Works (Step-by-Step)

1. Created as a Cook Islands Trust from Inception

The trust is legally established under the Cook Islands International Trusts Act from the moment it is formed.

This matters because asset-protection planning must exist before litigation becomes foreseeable.

Planning done before a claim arises is legitimate structuring.

Planning done after a claim appears can be treated as a fraudulent transfer.

⸻

2. “Bridged” Back to the United States for Tax Purposes

While administered domestically, the trust operates as a U.S. grantor trust under:

IRC §§ 671–677

IRC § 7701

Assets are managed domestically and reported under the grantor trust rules for U.S. tax purposes.

The structure is designed to be tax-neutral, not tax-avoidant.

⸻

3. Operates Domestically During Normal Conditions

During normal circumstances, the trust functions much like a domestic trust.

Assets are managed domestically while the offshore legal framework remains embedded in the governing instrument.

The offshore trustee relationship already exists — but remains dormant unless needed.

⸻

4. Transition Occurs Only if a Credible Threat Arises

If a serious legal threat appears, the trust may shift jurisdiction.

Examples may include:

• major lawsuits

• creditor enforcement actions

• judgments

• government investigations

The decision to transition offshore is not automatic.

⸻

5. Human Oversight Through an Independent Trust Protector

The decision to activate offshore administration is made by an independent Trust Protector exercising fiduciary judgment.

There are:

• no automatic triggers

• no pre-programmed switches

• no hidden transfers

Every step is deliberate and legally supervised.

This design preserves compliance while ensuring the offshore defense remains available when justified.

Is the Bridge Trust® Legal?

Yes.

The Bridge Trust® relies on two well-established legal frameworks:

• Cook Islands trust law for asset-protection jurisdiction

• U.S. grantor-trust tax law for IRS transparency

When structured and funded before litigation is foreseeable, this hybrid approach is fully lawful and court-defensible.

⸻

The Statutory Power Behind the Bridge Trust®

The Cook Islands International Trusts Act (1984, as amended) is widely considered the strongest asset-protection trust statute in the world.

Key protections include:

1. Non-Recognition of Foreign Judgments

U.S. judgments are not enforceable in the Cook Islands.

Creditors must re-litigate claims locally.

⸻

2. Criminal-Level Burden of Proof

Fraud must be proven beyond a reasonable doubt — the highest civil burden in any jurisdiction.

The creditor must also prove the transfer rendered the settlor insolvent.

⸻

3. Strict Limitation Periods

Claims must be filed:

• within 1 year if the claim arose within two years of the transfer

• within 2 years otherwise

After that period, claims are permanently barred.

⸻

4. Duress and Relationship-Property Protections

Cook Islands trustees are prohibited from complying with foreign court coercion or repatriation demands.

These protections were strengthened through legislative amendments between 2021–2023.

⸻

5. Long-Term Trust Duration

Cook Islands trusts may last 100 years or longer, supporting long-term and multigenerational planning.

This is real offshore law — not marketing language.

⸻

Case Law and Offshore Trust Enforcement

Courts do not defeat properly structured offshore trusts simply because they are offshore.

Most failures occur when:

• planning is reactive

• the settlor retains improper control

• transfers are fraudulent

Key cases illustrate this principle.

FTC v. Affordable Media (Anderson)

The Anderson case demonstrated the difficulty of enforcing U.S. court orders against assets controlled by an independent Cook Islands trustee.

⸻

SEC v. Solow (2010)

The court recognized that inability to repatriate assets is not fraud when the settlor lacks control.

⸻

U.S. v. Grant and Reichers v. Reichers

These cases acknowledged legitimate uses of offshore trusts for asset preservation when properly structured.

The reason you rarely hear about successful offshore trust challenges is itself worth understanding.

⸻

Offshore Enforcement Reality

Creditors can attempt enforcement — but the economics often make it impractical.

Typical barriers include:

• Bond requirements of roughly $50,000 USD

• Fee-shifting where the losing party pays both sides

• High burden of proof

• Short limitation periods

As a result, many claims fail long before trial.

⸻

Why Domestic Asset Protection Trusts Often Fail

Domestic Asset Protection Trusts (DAPTs) rely on state statutes that attempt to shield self-settled trusts from creditors.

However, U.S. courts frequently apply the law of the debtor’s home state rather than the trust state.

Examples include:

• In re Huber (2013)

• Battley v. Mortensen (2011)

• Dahl v. Dahl (2015)

• Toni 1 Trust v. Wacker (2018)

• United States v. Huckaby, (2026)

• Kilker v. Stillman (2012)

These cases demonstrate that domestic jurisdiction often overrides DAPT statutes.

When People Usually Start Looking for a Bridge Trust®

Most clients do not begin researching asset protection randomly.

They start looking after something raises their awareness of risk.

Common triggers include:

• building a large real-estate portfolio

• signing personal guarantees on business debt

• receiving a malpractice claim or legal threat

• selling a business and accumulating liquid wealth

• realizing insurance coverage may not fully protect them

These moments are often the first time people ask a simple question:

“If something serious happens, are my assets actually protected?”

That question is exactly what the Bridge Trust® was designed to answer.

⸻

IRS, FinCEN, and Reporting Compliance

The Bridge Trust® is tax-neutral, not tax-avoidant.

Relevant compliance rules include:

• IRC §§ 671–677 and § 7701

• Treas. Reg. § 1.671-1 and § 1.671-4

• Forms 3520 and 3520-A if the trust transitions offshore

• FBAR (FinCEN Form 114)

• FATCA reporting where applicable

There is no secrecy.

Only lawful jurisdictional separation.

⸻

Who the Bridge Trust® Is (and Is Not) For

Well-Suited For

• physicians and surgeons

• real-estate investors

• entrepreneurs with personal guarantees

• high-liability professionals

⸻

Not Appropriate For

• individuals already in litigation

• fraudulent transfers

• tax evasion schemes

• last-minute planning

Timing matters.

⸻

Bridge Trust® FAQs

Is the Bridge Trust® the same as an offshore trust?

No. It is offshore in legal foundation but domestic in tax operation until a transition occurs.

⸻

Does it avoid U.S. taxes?

No. All income remains fully reportable under U.S. tax law.

⸻

Can U.S. courts force repatriation?

Only when the settlor retains improper control or commits fraud.

Where control rests with an independent trustee, enforcement becomes far more difficult.

⸻

Is the Bridge Trust® a Domestic Asset Protection Trust?

No. It does not rely on U.S. DAPT statutes.

⸻

Who decides when the trust goes offshore?

An independent Trust Protector, not an automated trigger.

⸻

For Ultra-High-Net-Worth Families: The Dynasty Bridge Trust™

The Bridge Trust® solves the problem most high-net-worth professionals face — protecting what they have built from a serious creditor threat during their lifetime.

But for families with $12 million or more in exposed assets, there is a second problem that the Bridge Trust® alone was not designed to address. What happens to those protected assets after you are gone?

A standard estate plan transfers your wealth. It does not defend it. The moment your children inherit outright — under a revocable living trust, a will, or any conventional distribution mechanism — those assets immediately re-expose to everything in your heirs’ lives. Their creditors. Their divorcing spouses. And estate taxes that can take up to 40 percent at every generational transfer, eroding what you built across decades in a single inheritance event.

The Dynasty Bridge Trust™ is the answer to that second problem.

It combines the Bridge Trust® offshore protection architecture — Cook Islands jurisdiction, independent Trust Protector, Event of Duress mechanics — with downstream Nevada dynasty subtrusts that protect your heirs from their own exposure after you are gone. The subtrusts are governed by Nevada law, which has eliminated the Rule Against Perpetuities entirely. That means the structure can hold and compound your family’s wealth indefinitely, across every generation, without estate tax triggered at each transfer.

Your children benefit from the assets. They simply do not own them outright. And because they do not own them outright, a creditor suing your son cannot reach what is in his subtrust. His divorcing spouse cannot claim it as marital property. The GST exemption is allocated at funding, sheltering all future appreciation from generation-skipping transfer tax as wealth moves across generations.

The result is a structure that covers both timelines simultaneously.

During your lifetime: the Bridge Trust® with its Cook Islands offshore capacity defends your assets from creditor claims. After your death: the dynasty subtrusts defend your family’s inheritance from their own exposure and eliminate the estate tax erosion cycle.

Most advisors address these as two separate conversations handled by two separate attorneys with two separate structures. The Dynasty Bridge Trust™ closes both gaps in one integrated system.

If you are evaluating the Bridge Trust® and your estate exceeds $12 million, the Dynasty Bridge Trust™ deserves a place in that conversation.

Conclusion:

Structure Before Stress

The Bridge Trust® is not a theory.

It is a statute-anchored, compliance-first asset-protection system designed for the modern litigation environment.

Asset protection always comes down to three things:

Timing. Control. Jurisdiction.

You only get one opportunity to structure your assets before a legal crisis appears.

Make sure your structure exists before you need it.

📞 For a confidential legal consultation with an Asset Protection Attorney, contact Bradley Legal Corp. at (888) 773-9399 or visit btblegal.com.

By: Brian T. Bradley, Esq.

Asset Protection Attorney | Bradley Legal Corp.