A financial planner I have worked with for years called me last month. One of his clients — a married couple with operating businesses, real estate, and a balance sheet in the $10 million to $30 million range — had just come out of a meeting with a well-known transfer-tax attorney at an AmLaw 200 firm. The proposal in front of them was elegant. Paired Nevada irrevocable trusts. Formula valuation clauses to defend against IRS challenge. Full deployment of the couple’s combined estate tax exemption. A long-term dynasty trust planning structure for the grandchildren. The clients were impressed. The planner was not.

He could not name what was wrong. The firm was respected. The structure was sophisticated. The presenting attorney was confident. But something about the proposal kept bothering him, and he finally said it the way an experienced advisor says it when his instincts are firing without language yet attached.

“Brian, it feels like they’re being asked to commit to a lot all at once. Can you take a look at this for me before they sign anything.”

That instinct was correct. And the reason he caught it — and the reason most clients do not — is exactly what almost no one explains to families sitting in those meetings.

The estate planning landscape changed materially in 2025, and the planning conversations that follow have to account for that change. For the better part of a decade, the dominant frame in transfer-tax planning was the approaching sunset — deploy exemption now, before the rules change, before the cliff arrives. That frame was rational and well-grounded in the law as it stood. What has shifted is not whether urgency can ever apply, but whether urgency applies to a given family’s specific situation. The math is now case-by-case in a way it was not before.

What the OBBBA Actually Changed

On July 4, 2025, Congress enacted the One Big Beautiful Bill Act. It permanently set the federal estate, gift, and generation-skipping transfer tax exemption at $15 million per individual and $30 million per married couple, effective January 1, 2026. The exemption is indexed to inflation beginning in 2027, with 2025 as the base year.

The word that matters in that paragraph is permanent.

Before the OBBBA, the Tax Cuts and Jobs Act exemption was scheduled to sunset at the end of 2025. If Congress did nothing, the exemption was going to drop by roughly half on January 1, 2026. That sunset was the engine of the entire “use it or lose it” estate planning conversation for eight years. Every paired trust pitch, every dynasty trust deployment, every aggressive front-loaded gift was framed against the cliff. The cliff is gone.

To reduce the exemption now requires affirmative new legislation. That is a different political dynamic than letting an existing sunset expire automatically. It can happen — Congress can change anything — but it is no longer the default. The default is now the $30 million couple exemption, growing with inflation, sitting available for the family to deploy whenever the math actually justifies it.

For families above $30 million, the case to deploy now can be strong. Appreciation lock-in, GST portability gaps, generation-skipping leverage, and the political risk of future legislation are real arguments and well-supported on the right facts.

For families at or below $30 million, the math is more nuanced. The legislative cliff that drove much of the pre-2026 urgency framing is no longer in the calculus, which means the affirmative case for deployment now has to rest on the family’s specific position — appreciation profile, asset mix, succession timeline, current creditor exposure — rather than on the timing of a sunset that no longer exists. The question is no longer how do we beat the sunset. The question is what should we commit to today, and what should we preserve as a decision we can make later when we know more.

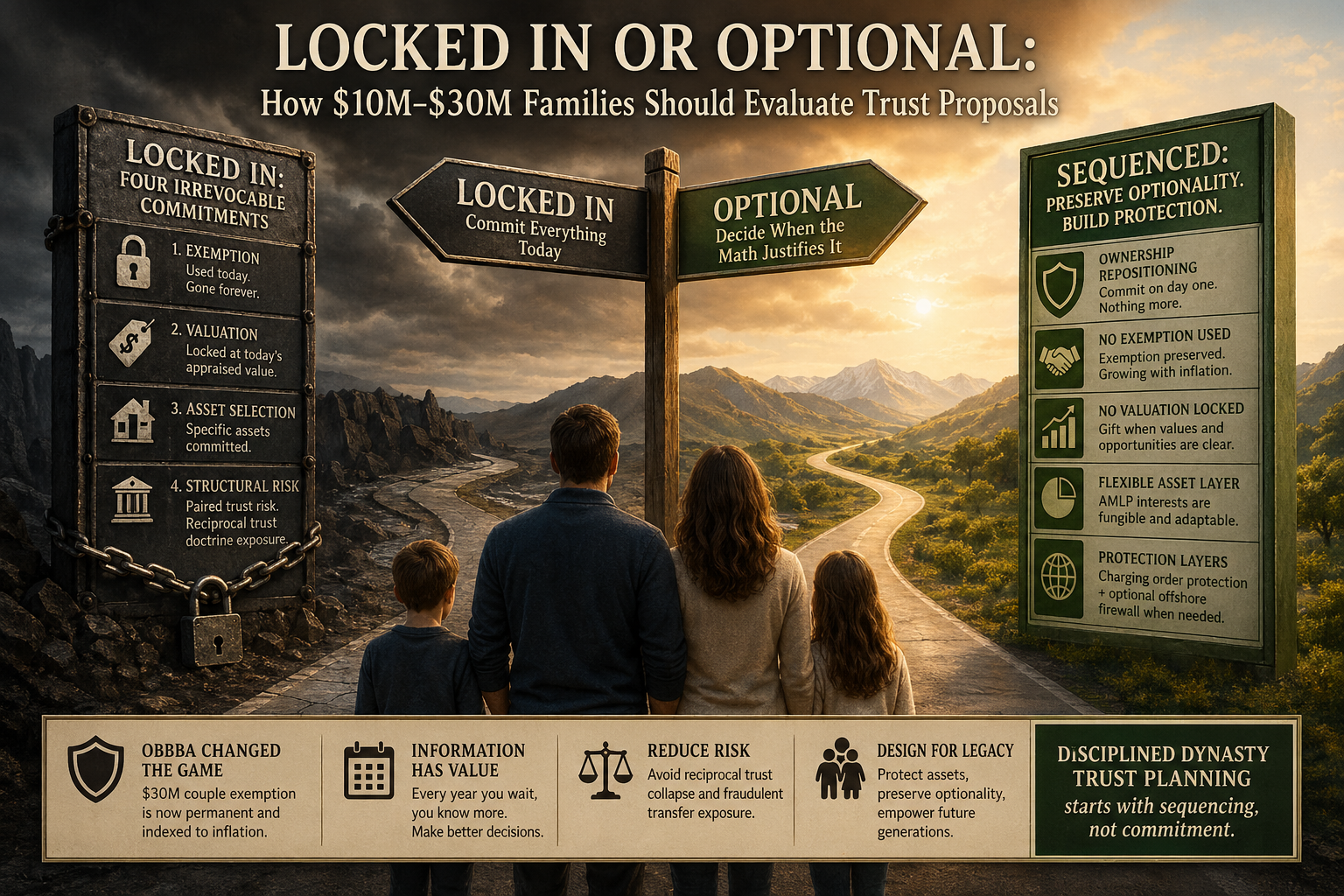

The Four Irrevocable Commitments Most Plans Force

When a family executes a typical paired-trust gifting structure, they make four separate commitments on the same day. Each one is irrevocable. Each one has consequences that can take decades to play out. And almost no one walks the family through what each commitment actually costs.

The first commitment is exemption. When the gift hits Form 709, the exemption is used. Whatever amount the family deploys today is gone. They cannot reclaim it if circumstances change. They cannot redirect it to a different trust, a different beneficiary, or a different time. If the family deploys $20 million of combined exemption into the structure this year, they have committed two-thirds of their lifetime capacity to one decision made on one day. The remaining $10 million they did not use is still available, but the deployed portion is fixed.

The second commitment is valuation. The whole point of the formula clause defense — the Wandry and Petter and McCord line of authority — is to lock in today’s appraised value of the transferred interests. If the family is gifting closely held LLC units or partnership interests at a 30 percent valuation discount, that discount is calibrated to what the assets are worth right now. If those assets double in value next year, the family captured the gift at the lower number. Good outcome. If those assets crash next year, they used exemption against an inflated value. Bad outcome. Either way, the valuation is committed and the appraisal is on file.

The third commitment is asset selection. Specific assets land inside the trust. A 50 percent interest in the operating company. A piece of real estate. A concentrated stock position. Once the gift is complete, those particular assets are owned by the trust, not by the family. Removing them, swapping them, or unwinding them requires either a substitution power that has its own tax mechanics or a trust modification process that can be expensive, slow, and sometimes impossible. The family cannot simply say we want to sell that property next year and use the proceeds for something else without engaging trust mechanics that the structure was not designed to make easy.

The fourth commitment is structural. The paired Nevada trusts exist. The trustee fees are running. The administrative burden is locked in. The reciprocal trust risk under United States v. Estate of Grace, 395 U.S. 316 (1969), is now baked into the family’s estate plan. If a court ever applies the reciprocal trust doctrine — and California courts have applied substantially similar analysis to Nevada trusts — the structure can collapse on itself in ways the family did not anticipate when they signed the engagement letter.

All four commitments happen on day one, before the family knows whether any of them will turn out to be the right call. That is what locked in means.

Sequencing as Disciplined Dynasty Trust Planning

There is a different way to think about this, and it starts from a different question. Instead of asking what is the most aggressive transfer-tax position we can take today, ask what does the family actually need to do today, and what should they preserve as a decision they can make later when they know more.

The architecture that flows from that question executes only one commitment on day one. Ownership repositioning. Nothing more.

A foundational dynasty trust gets created — irrevocable, drafted as a long-duration trust under Nevada law (NRS 111.1031 supports trust durations up to 365 years), with generation-skipping transfer tax exemption allocated to preserve future capacity. The trust holds an Asset Management Limited Partnership organized under Arizona law. Arizona’s limited partnership statute (A.R.S. § 29-3503) makes the AMLP charging-order exclusive — a creditor of a partner gets a charging order against distributions only, never an attachment of the underlying interest, never forced liquidation. The AMLP becomes the holding entity for the family’s investment assets. The Bridge Trust® holds the AMLP interests as a U.S. grantor trust under IRC §§ 671–677, with pre-registered Cook Islands offshore capacity that activates only when a credible legal threat materializes. The Trust Protector controls when and how that offshore migration occurs.

What the family commits to on day one: ownership repositioning into the structure. What the family does not commit to on day one: any of the four irrevocable decisions a paired-trust gifting structure forces.

No exemption is used. The exemption sits available, growing with inflation, ready to deploy when the math justifies it. No valuation is locked in. Appraisals can be obtained over time, with multiple data points across multiple years, when the family actually decides to gift. No specific assets are committed to permanent trust ownership beyond what is necessary to populate the AMLP. The LP interests are fungible. The family can sell the underlying real estate, restructure the operating business, swap one investment for another — all without engaging the trust mechanics that a completed gift would lock in. No paired-trust structural risk exists. There is one foundational dynasty trust, not two mirror-image trusts on each side. The reciprocal trust doctrine has nothing to uncross.

The LP layer becomes what I call the optionality engine. Because LP interests can be transferred in fractional amounts, the family retains the ability to implement gifting later, in a controlled and deliberate way. If the exemption drops by future legislation, they can deploy. If their asset base grows meaningfully, they can deploy on the appreciation. If they want to gift to a specific child or grandchild for a specific purpose at a specific time, they can deploy that fraction. If they want to gift nothing, they do nothing. The structure supports both outcomes.

Every year that passes, the family gets more information. About asset values. About legislation. About their own circumstances. About their heirs. About creditor exposure. That information has economic value, and the sequencing approach lets the family use that information when making transfer decisions. The locked-in approach forces every decision before that information is available.

For families operating in any other domain where uncertainty exists, this would be obvious. No one would advise a portfolio manager to liquidate every position on day one because prices might go down. No one would tell a buyer to sign every contract before due diligence because the seller might raise the price. Optionality has positive value when the future is uncertain, and the future is always uncertain.

The Risks That Compound Locking In

There are two specific risks that compound the case against premature gifting structures, and they show up in the case law more often than the marketing materials suggest.

The first is reciprocal trust collapse. When two spouses each create substantially similar trusts naming each other as beneficiaries — same year, similar structures, similar timing, similar funding — the Supreme Court’s framework in United States v. Estate of Grace says the trusts can be uncrossed and each spouse treated as the settlor of the trust they actually benefit from. That collapse converts a third-party-settled structure into a self-settled structure. On California facts, it triggers Cal. Probate Code § 15304’s anti-self-settled rule, which lets creditors reach what could be distributed to the settlor-beneficiary despite the spendthrift clause.

This is not theoretical. California courts have applied this analysis to Nevada trusts. In Kilker v. Stillman, 233 Cal. App. 4th 320 (2015), the California Court of Appeal declined to enforce a Nevada self-settled trust against a California judgment creditor. More recently, the Huckaby decision in 2026 reinforced this framework — the court allowed Nevada law to govern trust construction but applied California situs law to creditor access against California real property held in the trust. Because the debtors were settlors, trustees, and sole lifetime beneficiaries, § 15304 made the spendthrift restraint ineffective and the federal judgment lien attached. The Nevada governing-law clause did not save the structure. I walked through this framework in detail in my analysis of self-settled spendthrift trusts in California.

The second risk is fraudulent transfer optics. When a family makes a large gift close in time to any potential claim, the transfer becomes vulnerable under Cal. Civ. Code § 3439 et seq., the Uniform Voidable Transactions Act. The badges of fraud analysis under § 3439.04(b) — insider transferee, retention of control, concealment, threat of suit, transfer of substantially all assets — can apply even when the family had no specific creditor in mind at the time of the gift. A creditor that arises within four years of the transfer (seven years for actual fraud, with a discovery extension) can move to set the transfer aside.

The sequencing approach avoids that exposure entirely. No gift is made at the front end. The family is repositioning ownership into a protected structure, not transferring value out of their estate. There is no fraudulent transfer to attack, because there is no transfer. When the family does decide to gift later — through fractional LP transfers calibrated to current circumstances — the gifts can be timed and sized to avoid any creditor proximity issues.

These two risks compound. A paired-trust structure that gets reciprocal-trust-collapsed and attacked under UVTA is a double failure. The sequencing structure has neither vulnerability.

The Diagnostic the Family Should Run

The right way to evaluate any trust proposal is to ask the family, not the lawyer, the following question. What do you actually know today about your estate, your assets, your heirs, the legislative environment, and your future creditor exposure — and what would you prefer to decide later, when you know more?

If the family is sitting at $50 million with concentrated growth assets, a clear succession plan, established heirs, and a stable creditor profile, the case for executing transfer-tax planning aggressively today is strong. There is enough capacity, enough appreciation potential, and enough certainty about the family’s structure to commit. The locked-in approach makes sense.

If the family is sitting at $10 million to $30 million, with operating businesses whose values fluctuate, with children whose paths are not yet clear, with grandchildren who are still young, with potential liability exposure from active operations, and with no immediate legislative cliff to beat — the case for executing aggressively today is much weaker. The optionality approach makes more sense, because the family does not yet have the information they need to make several of those four irrevocable decisions well.

The question is not whether the proposed structure is sophisticated. The diagrams from the AmLaw 200 transfer-tax firms are sophisticated. The question is whether the structure matches the family’s actual position, the actual exposure profile, and the actual timeline they are operating on.

What This Means for the Reader

If you are the reader who walked out of an estate planning meeting this month with a paired Nevada trust proposal in hand, the questions to bring to your next conversation are these.

Why am I being asked to use my exemption today rather than later?

What information will I have in three years that I do not have now, and would that information change the decision I am being asked to make?

If the exemption is permanent and growing with inflation, what is the urgency case for executing today?

What does the structure cost me in optionality if circumstances change?

What does the structure cost me in protection if a creditor arises before I have completed the gifts?

If the answers do not satisfy you, the proposal may be solving a problem the family does not have, while leaving the problem the family does have — operating-business liability, real-estate exposure, concentrated wealth — completely unaddressed. The full architecture of how a layered Bridge Trust® and dynasty trust planning approach solves both problems is something I have written about in detail at California Families’ Generational Tax Problem.

The instinct the financial planner had on that call was right. A sophisticated structure is not the same as the right structure. And committing to four irrevocable decisions on the same day, before the family has the information needed to make any of them well, is not disciplined planning. It is the appearance of planning, applied without regard to whether the family’s actual position requires it.

Disciplined dynasty trust planning starts with sequencing, not commitment. Structure before stress. And optionality before commitment.

Frequently Asked Questions:

Should I use my estate tax exemption now or wait?

It depends on the size of your estate, the appreciation profile of your assets, and your tolerance for irrevocable commitment. For estates above the current $30 million couple exemption with rapidly appreciating assets, deployment today often makes sense. For estates at or below the exemption, the case for waiting is usually stronger now that the OBBBA permanently locked the exemption with inflation indexing. The decision should be made on the math, not on urgency that no longer applies.

What did the OBBBA change about estate tax exemption?

The One Big Beautiful Bill Act, enacted July 4, 2025, permanently set the federal estate, gift, and GST exemption at $15 million per individual and $30 million per married couple, effective January 1, 2026, with inflation indexing beginning in 2027. It eliminated the scheduled sunset that would have reduced the exemption by roughly half. Reducing the exemption now requires new legislation, not automatic operation of law.

What is the difference between a SLAT, a SLANT, and a Dynasty Bridge Trust™?

A SLAT (Spousal Lifetime Access Trust) is a grantor trust where one spouse gifts to a trust for the other spouse and descendants. A SLANT (Spousal Lifetime Access Non-Grantor Trust) is the same structure but drafted to be non-grantor for income-tax purposes, typically using an adverse-party distribution committee. A Dynasty Bridge Trust™ is a layered architecture combining a long-duration dynasty trust, an Arizona Asset Management Limited Partnership for charging-order protection, and pre-registered Cook Islands offshore capacity for jurisdictional firewall when activated. The first two are estate-tax tools. The third does both estate-tax and asset protection in a sequenced way.

What is the reciprocal trust doctrine?

When two spouses each create substantially similar trusts naming each other as beneficiaries, the IRS or a creditor can ask a court to “uncross” the trusts and treat each spouse as the settlor of the trust they actually benefit from. The doctrine originated in United States v. Estate of Grace, 395 U.S. 316 (1969), and applies when the trusts are interrelated and leave the spouses in approximately the same economic position they were in before. The collapse converts a third-party trust into a self-settled trust, which California refuses to honor under Cal. Probate Code § 15304.

Is my estate too small for sophisticated trust planning?

No estate is too small for asset protection. Operating businesses, real estate, and concentrated investments create liability exposure regardless of estate size. The question is what kind of planning matches your situation. Below $30 million, transfer-tax-driven gifting structures often impose costs (committed exemption, locked valuations, lost optionality) that exceed their benefits. Asset-protection-driven dynasty trust planning structures that defer gifting decisions until they are clearly justified can deliver protection without forcing premature commitment.

Can I undo a Dynasty trust if I change my mind?

Generally not. Dynasty trusts are irrevocable by design — that is what makes them work for transfer-tax purposes. Some structural flexibility exists through trustee discretion, decanting under state law, and trust protector powers. But the core decisions made at funding (exemption use, valuation, asset selection) are irrevocable. That is precisely why the timing of when to execute these decisions is the most important strategic question in the entire conversation.

If you are evaluating a trust proposal and want a structured second opinion, my office offers a 30-minute legal consultation focused on whether the proposed structure matches your actual exposure profile, asset mix, and family timeline.

Call today for a legal consultation with an asset protection lawyer at (888) 773-9399

By: Brian T. Bradley, Esq.

Structure before stress