A business owner in Chicago had done everything right — or so he believed. His estate planning attorney had drafted an irrevocable Dynasty Trust, named his children as beneficiaries, and assured him that the structure would protect his assets across multiple generations. The trust was sitused in Nevada. It had a spendthrift clause. It had a professional trustee. It had a Trust Protector. On paper it looked exactly like what a sophisticated multi-generational wealth plan should look like.

What it did not have was genuine separation between him and the trust assets. He had retained the right to receive distributions at the trustee’s discretion. The trustee was a close associate. He had funded the trust with assets accumulated during a period when a significant business dispute was already on the horizon.

When the creditor’s attorney finished discovery, none of the trust structure mattered. The court applied Illinois law. The trust was effectively self-settled. The spendthrift provisions were void as to his creditors under 760 ILCS 3/505. The assets he had placed in the trust were reachable.

The problem was not the trust. The problem was the misunderstanding of what a Dynasty Trust actually does — and what it does not do — for the person who funded it.

Dynasty Trusts are among the most powerful tools in estate planning and tax mitigation. They are not, by themselves, a comprehensive asset protection strategy for the person who creates them. Understanding that distinction before a threat appears is the difference between a structure that holds and one that collapses under pressure.

What Is a Dynasty Trust and What Does It Actually Do Well?

A Dynasty Trust is an irrevocable trust designed to hold assets across multiple generations without triggering estate taxes at each generational transfer.

In jurisdictions without a Rule Against Perpetuities — including Nevada, South Dakota, Delaware, and Alaska — these trusts can theoretically hold assets indefinitely.

The estate planning and tax mitigation benefits are genuine and substantial. A well-drafted Dynasty Trust eliminates estate taxes on the assets held inside it at each generational transfer. It allows the trustee to sprinkle income to beneficiaries in lower tax brackets, reducing the overall federal income tax burden on the family.

In states without income taxes on trust income — or through careful siting of the trust — it can reduce or eliminate state income tax on accumulated earnings. And through sophisticated basis planning at death, an independent trustee or Trust Protector can selectively provide step-ups in basis for appreciated assets without triggering step-downs on depreciated ones.

For beneficiaries who receive distributions from a properly structured third-party Dynasty Trust, the protection from their own creditors is also genuine. A child who receives a discretionary distribution from a Dynasty Trust funded by a parent is in a fundamentally different legal position than a child who inherits the same assets outright.

Outright inheritance immediately exposes those assets to the child’s creditors, their divorcing spouse, and any judgment entered against them. The trust holds that exposure at bay for as long as assets remain inside it.

This beneficiary-level protection is one of the most compelling non-tax reasons to use a Dynasty Trust. It is real. It works. And it is entirely consistent with centuries of well-established trust law.

The confusion arises when the person who funded the trust assumes those same protections apply to them.

What Does a Dynasty Trust Not Do for Asset Protection Purposes?

The foundational rule of asset protection trust law has not changed in centuries: a person cannot place assets into a trust for their own benefit and simultaneously shield those assets from their own creditors. This is the self-settled trust doctrine. It applies in every high-litigation state in the country. And it applies to Dynasty Trusts as directly as it applies to any other structure.

Restatement (Second) of Trusts §156 codifies the principle: where the settlor is also a beneficiary, restraints on alienation are ineffective as to the settlor’s creditors, even when the trust itself remains valid. The trust does not disappear. The spendthrift clause does not disappear. But as to the settlor’s own creditors, the protective provisions are void to the extent of the maximum amount the trustee could distribute to the settlor.

Dynasty Trusts extend this analysis intergenerationally but do not change it. If a beneficiary of a Dynasty Trust is treated by a court as the effective settlor — through direct self-settlement, alter-ego theories, fraudulent transfer analysis, or retained control doctrines — that beneficiary’s interest is exposed. The multi-generational holding structure does not convert a self-settled arrangement into a protected one.

Modern DAPT jurisdictions — Nevada, Alaska, Delaware, South Dakota — created statutory exceptions to the self-settled rule.

But those exceptions only apply when the forum court honors the DAPT state’s law. In high-litigation states like California, New York, Florida, Texas, and Illinois, that is precisely what courts refuse to do.

The Three Questions That Determine Whether a Dynasty Trust Protects You

Before any analysis of specific state law, three threshold questions determine the asset protection posture of any Dynasty Trust structure.

First: Is the settlor a beneficiary? If yes, the self-settled trust doctrine applies in every high-litigation state. The settlor’s beneficial interest is reachable by creditors to the maximum amount distributable to or for the settlor, regardless of what the trust document says about spendthrift protection.

Second: Is the trust sitused entirely in U.S. jurisdiction? If yes, a U.S. court with personal jurisdiction over the settlor or beneficiary can reach the assets. The protection ceiling for any domestically sitused trust is the willingness of the forum state’s courts to honor the trust’s chosen law — and in California, New York, Florida, Texas, and Illinois, that willingness is severely limited when the settlor has connections to the forum state.

Third: Are the assets held directly in the trust or layered through entities? If held directly, the law of the situs of the underlying assets controls creditor rights — as United States v. Huckaby, 2026 WL 587784 (E.D. Cal. Mar. 3, 2026) just confirmed at the federal level. California real estate inside a Nevada trust is governed by California creditor law, not Nevada’s asset protection statute.

If a Dynasty Trust fails any one of these three questions, its asset protection value for the settlor is materially compromised. State law determines how completely it fails. Here is what the law says in each of the five highest-litigation states.

California: Probate Code §15304 and the Absolute Bar on Self-Settled Protection

California has the most straightforward and most hostile framework for self-settled trust planning of any major state. California Probate Code §15304(a) provides that if the settlor is a beneficiary of a trust created by the settlor and the interest is subject to a restraint on transfer, the restraint is invalid as against the settlor’s creditors. The trust itself remains valid. The spendthrift clause remains in place for other beneficiaries. But as to the settlor’s own creditors, the protection is completely void.

The California legislature reaffirmed this position in AB 1866 (2023), which added §15304(c) to clarify that a trustee’s ability to reimburse a settlor for income taxes does not create a creditor-accessible beneficial interest. It was a tax clarification — not an asset protection loophole.

Federal courts applying California law have consistently enforced this framework. In re Cutter, 398 B.R. 6 (B.A.P. 9th Cir. 2008), held that a debtor-settlor’s beneficial interest in a California spendthrift trust is reachable by creditors and the bankruptcy estate to the maximum distributable amount, regardless of spendthrift language. In re Bogetti (9th Cir. BAP 2023) reiterated the same principle under current law.

The most significant recent development is United States v. Huckaby, 2026 WL 587784 (E.D. Cal. Mar. 3, 2026). The court applied Restatement (Second) of Conflict of Laws §280 to hold that creditor rights against California real property are governed by California law — not by the law of the state where the trust was registered. A Nevada-designated trust holding California real estate did not receive Nevada’s asset protection treatment. California law controlled. The self-settled doctrine applied. The IRS lien attached and foreclosure was authorized.

Huckaby confirms what Kilker v. Stillman established in 2012: a California resident cannot use an out-of-state trust registration to import asset protection laws that California has explicitly rejected. The principle is not new. The federal authority is.

United States v. Harris, 942 F.3d 1011 (9th Cir. 2019), extends this analysis to federal restitution liens against discretionary trust distributions. The Ninth Circuit held that a California debtor’s right to receive distributions under California law constituted “property” for federal lien purposes, and spendthrift clauses did not prevent attachment of a writ of continuing garnishment to current and future distributions. Practitioners read Harris as a warning that even third-party discretionary Dynasty Trusts in California may not block federal tax or restitution liens from reaching the distribution stream.

For California-based Dynasty Trust planning, the framework is unambiguous. Third-party Dynasty Trusts — where the California resident is a beneficiary but not the settlor — receive robust spendthrift protection against private creditors. Self-settled arrangements receive none. And federal creditors present a separate layer of exposure that reaches even discretionary distribution rights under Harris.

New York: EPTL §7-3.1 and the Statutory Prohibition on Self-Settled Protection

New York’s prohibition on self-settled trust protection is statutory and absolute. New York Estates, Powers and Trusts Law §7-3.1 provides that a disposition in trust for the use of the creator is void as against existing and subsequent creditors of the creator. Unlike California’s §15304, which voids only the restraint on transfer while leaving the trust intact, New York’s provision voids the disposition itself as to creditors — a more aggressive formulation.

The Portnoy and Brooks line of federal bankruptcy cases illustrates how New York courts treat out-of-state DAPT registrations. In both cases, bankruptcy courts applying Restatement (Second) of Conflict of Laws §270 declined to apply asset-protection-friendly situs law and instead applied New York law as the jurisdiction with the dominant relationship to the debtor. The self-settled trust doctrine applied. The trust assets entered the bankruptcy estate.

For New York Dynasty Trust planning, the result is the same as California’s: third-party Dynasty Trusts with genuine separation between the funding generation and the beneficiary generation receive strong spendthrift protection against private creditors. Self-settled structures do not. And the public policy argument against honoring out-of-state DAPT law is well-established in New York courts, giving creditors a reliable path to challenge Nevada or Delaware trust registrations by New York-domiciled settlors.

Florida: §736.0505, Menotte, and the Limits of Offshore Planning

Florida Statute §736.0505 adopts a UTC-style creditor rights framework. For an irrevocable trust, a settlor’s creditor may reach the maximum amount that can be distributed to or for the settlor, regardless of whether there is a spendthrift clause.

Florida does not recognize domestic self-settled asset protection trusts. Any Florida-situs Dynasty Trust in which the Florida debtor is both settlor and beneficiary is transparent to the settlor’s creditors to the maximum distributable amount.

Menotte v. Brown, 303 F.3d 1261 (11th Cir. 2002), and In re Rensin, 600 B.R. 870 (Bankr. S.D. Fla. 2019), apply Florida policy to treat self-settled or effectively self-settled trusts — including offshore structures — as reachable by creditors or the bankruptcy estate when the Florida settlor retains significant benefits or control. The offshore registration does not immunize the structure when Florida’s courts apply Florida public policy to a Florida-domiciled debtor.

Olmstead v. FTC, 44 So.3d 76 (Fla. 2010), although focused on a single-member LLC, is consistently cited in Florida asset protection analysis as evidence of the Florida Supreme Court’s willingness to disregard formalistic structures and permit creditors to reach a debtor’s economic interest where the debtor effectively controls the entity. Courts transfer that reasoning readily to Dynasty Trust arrangements where the settlor-beneficiary retains meaningful operational control.

For Florida-based Dynasty Trust planning, the third-party trust structure remains protective for beneficiary-level protection. Self-settled arrangements fail under §736.0505. And Florida’s public policy framework, reinforced by Menotte and Olmstead, extends skepticism to offshore registrations when the debtor’s connections remain in Florida.

Texas: Property Code §112.035 and the Absence of a True DAPT Regime

Texas Property Code §112.035 authorizes spendthrift trusts and generally enforces spendthrift provisions against both voluntary and involuntary transfer of a beneficiary’s interest prior to distribution. Texas has historically respected third-party spendthrift trust protection.

What Texas does not have is a true DAPT regime. A Texas-resident settlor who funds a Dynasty Trust and retains a beneficial interest has no statutory basis for claiming asset protection against their own creditors. Texas courts treat the grantor’s retained interest as reachable by creditors despite spendthrift language, consistent with the Restatement (Second) of Trusts §156 baseline.

Recent Texas commentary highlights the use of turnover and receivership remedies as an additional enforcement tool. WC 4th & Colorado, LP v. Texas Capital Bank (2025) illustrates how Texas courts may use turnover orders to reach distributions or economic benefits when a debtor-beneficiary has meaningful control, particularly in closely held entity or family trust contexts. The Texas Business Organizations Code §§21.223 and 1.105 provide further creditor reach against trust and entity interests where the structure fails to maintain genuine separation between the debtor and the protected assets.

For Texas-based Dynasty Trust planning, discretionary third-party trusts are protective for beneficiary-level creditor claims. Self-settled arrangements are not protected. And Texas’s turnover and receivership framework gives creditors meaningful enforcement tools even against beneficial interests that have not yet been distributed.

Illinois: 760 ILCS 3/505 and Rush University v. Sessions

The Illinois Trust Code at 760 ILCS 3/505 adopts UTC-style rules directly: during the settlor’s lifetime, a settlor’s creditor may reach the maximum amount that can be distributed to or for the settlor under the terms of the trust, regardless of spendthrift language. Illinois does not recognize self-settled domestic asset protection trusts. The provision applies to both existing and future creditors.

Rush University Medical Center v. Sessions, 2012 IL 112906, is the most significant Illinois precedent on point. The Illinois Supreme Court applied the common law rule that a self-settled spendthrift trust is void as to existing and future creditors in the context of a donor who had moved nearly all assets into trusts — including offshore structures — after making a large pledge to Rush University. Although the court focused heavily on fraudulent transfer analysis, Sessions confirms that Illinois treats self-settled spendthrift trusts as ineffective against creditors and views aggressive self-settled trust planning with particular suspicion when a pre-existing obligation exists.

For Illinois-based Dynasty Trust planning, the framework mirrors the other high-litigation states: third-party Dynasty Trusts receive strong spendthrift protection for beneficiaries who did not fund the trust. Self-settled arrangements are void as to the settlor’s creditors under §505. And the Sessions analysis establishes that Illinois courts will apply this principle regardless of where the trust is registered if the debtor’s connections are in Illinois.

The Federal Overlay: Tax Liens, Restitution, and Bankruptcy

State law analysis only covers private civil creditors. Every Dynasty Trust in every state faces a separate and more powerful layer of creditor exposure from federal enforcement.

Under 26 U.S.C. §6321, the United States obtains a lien on all property and rights to property of a taxpayer once a federal tax assessment is made and demand is refused. Federal courts determine what constitutes “property” by reference to state law, but apply a broad federal standard once a property right exists. United States v. Craft, 535 U.S. 274 (2002), illustrates the Supreme Court’s willingness to treat state-law interests — in that case a joint tenancy interest that state law treated as non-alienable without spousal consent — as “property” for federal lien purposes.

United States v. Huckaby confirms this principle applies directly to trust beneficial interests. A settlor’s equitable title as beneficiary and legal title as trustee were both sufficient to attach the federal judgment lien, regardless of the Nevada spendthrift designation.

In bankruptcy, 11 U.S.C. §541(c)(2) preserves enforceable spendthrift restrictions for valid third-party trusts under applicable nonbankruptcy law. Where a Dynasty Trust is a genuine third-party structure with no self-settlement, this provision can protect the beneficiary’s interest from the bankruptcy estate. But where the trust is self-settled or functionally self-settled, the spendthrift restriction is not enforceable under the forum state’s law — and §541(c)(2) does not protect it. The beneficial interest enters the estate.

Federal bankruptcy courts applying Restatement (Second) of Conflict of Laws §270 have consistently looked past foreign choice-of-law clauses to apply the debtor’s home-state law in DAPT and offshore dynasty trust cases. The Portnoy and Brooks decisions in the New York bankruptcy courts, the Cutter and Bogetti decisions in the Ninth Circuit, and the Sessions analysis in Illinois all reflect a consistent judicial posture: where the debtor’s connections are in a non-DAPT forum state, that state’s law governs creditor rights.

What Asset Protection Looks Like When Combined With Dynasty Trust Planning

The limitations described above apply to Dynasty Trusts standing alone, sitused domestically, with the settlor retaining a beneficial interest. None of those limitations are inevitable. They are design problems with identifiable solutions.

A properly structured plan separates the estate planning function of the Dynasty Trust from the asset protection function of the layered structure that owns it. The Dynasty Trust’s multi-generational holding and tax efficiency benefits remain fully intact. The asset protection layer is built separately and correctly.

That means state-matched LLCs holding individual risk assets, owned by an Arizona Limited Partnership with charging order exclusivity under A.R.S. §29-3503, owned by a trust with a Cook Islands protection jurisdiction embedded in the governing instrument from formation. The settlor’s beneficial interest is separated from operational control through a genuine independent Trust Protector whose declaration authority is expressly not subject to judicial review. And the real estate — the asset most exposed to the situs rule confirmed in Huckaby — never sits directly inside any trust. It sits in a state-matched LLC, owned by the partnership, owned by the trust.

That layered structure addresses each of the three threshold questions directly. The settlor’s self-settled exposure is addressed through genuine control separation. The domestic situs problem is addressed through the Cook Islands jurisdictional anchor that operates outside the California-Nevada conflict of laws framework. And the direct asset placement problem is addressed by the LLC and partnership layers that stand between any trust creditor analysis and the underlying real estate.

The Dynasty Trust’s estate planning strength and the layered structure’s creditor enforcement resistance are not mutually exclusive. They address different legal questions and can coexist within the same overall holistic plan.

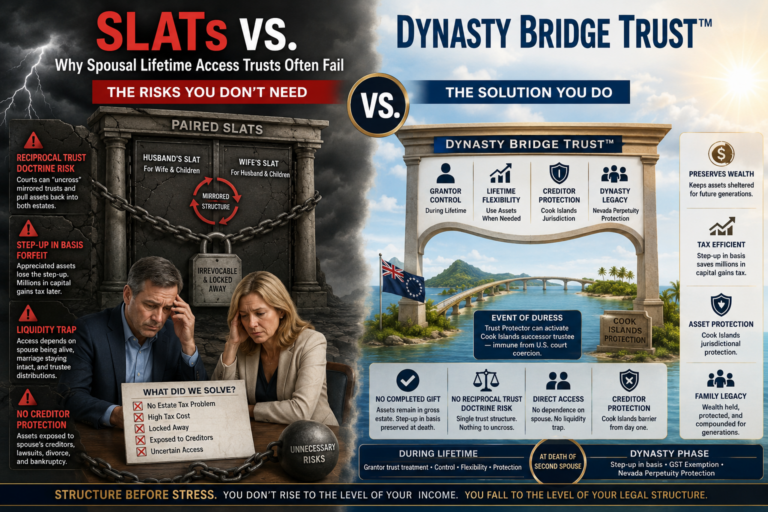

Dynasty Trust vs. Bridge Trust®: The Question Every Client Eventually Asks

Once a client understands what a Dynasty Trust cannot do for them personally, they ask the natural follow-up question: what is the difference between a Dynasty Trust and a Bridge Trust®? And can you build a Bridge Trust® that acts like a Dynasty Trust?

These are the right questions. The answers determine whether a client ends up with a plan that actually works or two tools that partially overlap and leave gaps in both directions.

What Problem Each Tool Is Designed to Solve

A Dynasty Trust is designed to solve an estate planning and tax efficiency problem. It holds assets across multiple generations, eliminates estate taxes at each transfer, shifts income to lower-bracket beneficiaries, and protects the assets of the next generation from that generation’s own creditors and divorcing spouses. The person it protects most directly is the beneficiary — a child, grandchild, or successor generation — not the person who funded it.

A Bridge Trust® is designed to solve a creditor enforcement problem for the person who creates it. It protects the settlor’s own assets from the settlor’s own creditors during their active earning and liability years. The offshore jurisdictional anchor, the independent Trust Protector EOD mechanics, and the layered LLC and partnership structure all exist to make collection against the settlor economically irrational and legally difficult. The person it protects most directly is the person who built it — the physician, the real estate investor, the entrepreneur who has something significant to lose right now.

- A Dynasty Trust protects your children from their creditors.

- A Bridge Trust® protects you from your creditors.

- They do not overlap. Both are necessary. Neither replaces the other.

When to Use a Dynasty Trust

Use a Dynasty Trust when the primary goal is multi-generational estate tax elimination and income tax efficiency. When you are transferring assets irrevocably to the next generation and want those assets protected from that generation’s creditors, divorcing spouses, and poor decisions. When the settlor has no significant personal creditor exposure during their own lifetime. When the client is in an estate tax bracket and the long-term compounding of estate tax elimination over 40 to 100 years justifies the structure’s complexity and cost.

A Dynasty Trust is the correct tool when the wealth transfer question is more urgent than the personal protection question. If your primary concern is ensuring that what you have built survives intact across three generations, a Dynasty Trust with proper third-party separation is the right structure for that objective.

When to Use a Bridge Trust®

Use a Bridge Trust® when the primary goal is protecting your own assets from your own creditors and lawsuits during your active earning and liability years.

When you are a physician, real estate investor, business owner, or entrepreneur with meaningful exposed net worth and real litigation risk right now.

When you need to maintain operational control of your assets during normal periods while having genuine offshore enforcement barriers available if you are attacked.

When you live in California, New York, Florida, Texas, or Illinois and domestic structures have documented failure rates against serious creditor claims.

The Bridge Trust® is the correct tool when the personal protection question is more urgent than the wealth transfer question. If your primary concern is ensuring that a lawsuit filed against you tomorrow does not reach the assets you have built, the Bridge Trust® with an AMLP and state-matched LLCs is the structure designed for that objective.

The Dynasty Bridge Trust™: When You Need Both

The question every serious client eventually arrives at is not which tool to choose. It is how to build a single cohesive plan that does both jobs without compromise.

The Dynasty Bridge Trust™ is the answer to that question. It is the Bridge Trust® — with its Cook Islands jurisdictional protection, independent Trust Protector EOD mechanics, and domestic grantor trust tax treatment — combined with the Arizona Limited Partnership, state-matched LLCs, and downstream Dynasty Trust distribution provisions that protect the next generation after the settlor’s death.

The structure works as follows. During the settlor’s active years, the Bridge Trust® with AMLP and LLCs provides the creditor enforcement barrier for the settlor’s own assets. The Cook Islands jurisdictional anchor is embedded from formation. The Trust Protector can declare an Event of Default if a serious threat appears, shifting administrative authority offshore where U.S. courts cannot reach. The settlor maintains operational control in the interim with no offshore reporting complexity during normal operations.

At the settlor’s death, the assets that pass through the Bridge Trust® structure flow into the Dynasty Trust subtrusts for children and grandchildren. Those downstream trusts are structured with genuine third-party separation — the beneficiary did not fund them, does not control them, and does not have unfettered access to them. The spendthrift protections are real. The beneficiary-level creditor protection, divorcing-spouse protection, and multi-generational holding mechanics of a properly structured Dynasty Trust apply fully at that stage.

The result is a structure that answers both questions a serious client needs answered. Who protects me from my creditors today? The Bridge Trust® with its offshore jurisdictional barrier. Who protects my children from their creditors after I am gone? The Dynasty Trust provisions in the downstream distribution architecture.

No gap between the two. No assets passing outright and immediately exposed. No generation receiving an inheritance that a plaintiff’s attorney can reach before the check clears.

The Dynasty Bridge Trust™ is not a compromise between estate planning and asset protection. It is both, built correctly, each layer doing its specific job without interfering with the other.

If you have been told you need to choose between protecting yourself today and protecting your family tomorrow, that is the wrong frame. The correct question is whether your structure addresses both — and whether it was built before the threat that will test it ever appeared.

The Bottom Line: Two Tools, Two Jobs, One Coherent Plan

Dynasty Trusts are exceptional estate planning and tax mitigation instruments. The intergenerational holding structure, the income shifting flexibility, the basis planning mechanics, and the beneficiary-level creditor protection are all genuine and well-established.

What they are not, in California, New York, Florida, Texas, or Illinois, is a comprehensive asset protection strategy for the person who funded them. The self-settled trust doctrine applies with full force in all five states. The conflict-of-laws framework allows those states’ courts to apply local law to out-of-state registrations. Federal tax liens and bankruptcy reach beneficial interests regardless of spendthrift designations. And the situs rule confirmed in Huckaby exposes assets held directly inside any domestic trust structure to the creditor law of the state where those assets are located.

The Bridge Trust® solves the problem the Dynasty Trust cannot solve — protecting the settlor’s own assets from the settlor’s own creditors, with a Cook Islands jurisdictional barrier that no U.S. court can reach, through an EOD mechanism that no TRO can freeze.

The practitioners who understand both tools build plans that use each for what it does. Dynasty Trust provisions for generational wealth transfer and beneficiary-level protection. Bridge Trust® with AMLP and LLCs for the settlor’s own creditor enforcement barrier during their active years. The two structures complement each other. Neither replaces the other. And a client who has both in place — properly structured, properly funded, and built before any threat appears — has addressed the full spectrum of what wealth protection actually requires.

Understand what each tool does. Use each for what it does well. Build the plan that closes both gaps. Structure before stress.

For a confidential legal consultation with an Asset Protection Attorney, contact Bradley Legal Corp. at (888) 773-9399

By: Brian T. Bradle, Esq. – National Asset Protection Attorney